Working Capital / Tied Capital

Leaning of working capital processes reduce interest expenses,

release capital and improve key figures!

Working Capital may be defined by efficiency of a company and their shortterm financial health. A positive working capital means that a company is theoretically

able to pay the shortterm liabilities. Nevertheless, with the requirement that

sufficient liquidity is available. Negative working capital means the respective

opposite.

Short Term Assets - Short Term Liabilities = Working Capital

(whereas short-term means with a remaining maturity of less than a year)

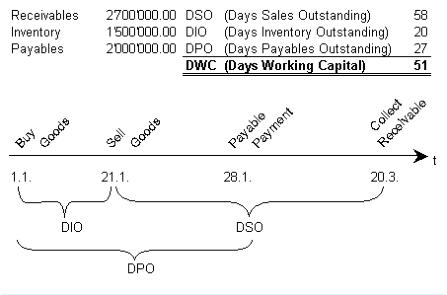

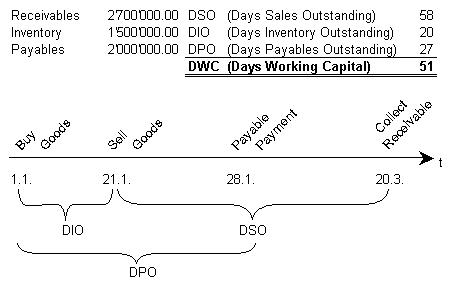

Terms, Key Performance Indicators

•

Days Sales Outstanding (DSO): Difference in days between invoice date and customer payment

•

Days Payable Outstanding (DPO): Difference in days between supplier invoice date and payment to supplier

•

Days Inventory Outstanding (DIO): Difference in days between invoice date of the supplier and the invoice to the customer for a specific good.

(Because the cash impact is not counting with the physical entry- or exit of the good in the warehouse. It is the invoice date of the supplier

invoice resp. invoice to the customer -> be aware of accruals!)

•

Days Working Capital (DWC) - Days, how long it needs to convert working capital in revenue. Also called “Cash Days”.

Calculation

1.

Direct Method: DSO - DPO + DIO = DWC

2.

Indirect Method: (WC[t2] - WC[t2] x 365 ) / Yearly Turnover = DWC

Example

With an assumed capital cost ratio of 8% the kpi’s of working capital

have these results:

DSO: 34'800.-

DIO: 6'666.67

DPO: -12'000.-

That equeals total costs of 29’466.67. Depending on further

circumstances these costs have also a direct impat to the liquidity.

The triggers for an optimization or trade receivables, trade payables

and mainly inventory turnover. For a sustainable success it is

mandatory to act strategic. That means, not just begging customers

for faster paymen or vendors for later payment. More from inside to

outside and thinking in clusters. Just this way a winning achievement

is possible. Are you interested how much your working capital cost and how much funds are locked? You will be surprised! Click here, in the

download area is a free excel tool to calculate those numbers.

Key Elements for Working Capital Management

•

Improvement of working capital unlocks frozen liquid funds, increase the free cash flow and reduce the inventory- and capital costs. (n.b. Free

Cash Flow = [Operating Cash Flow] + [Investment Cash Flow])

•

Consciously improvement of working capital processes release in average 20% - 30% tight capital.

•

The value of the company increase by re-investing the released funds. In consqueence the turnover rise what will lead to a better operational

cash flow by sametime reducing capital costs (same conditions assumed)

•

Working Capital is also an indicator for an upcoming crisis. If working capital rise faster than the turnover it means that more capital must have

been used that is at the end of the day just locked in operational processes. About three years before a liquidity crisis the ratio of [WC] /

[Balance Sheet Total] increase clearly.

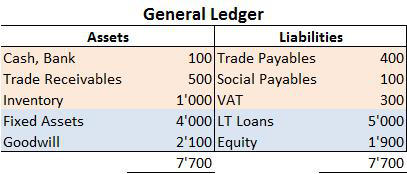

Managing Working Capital

Working Capital is per definition the short term part of a general ledger (see above). But it will be managed also by long term driven positions. Short

Term: operational processes (Purchase, Sales, Payments). Long Term: liquidity effective procedures like the disposal of fixed assets for cash or

repayment of long term liabilities and also change in equity for capital fund.

Approach for Improvment

A) Vendors

Don’t

•

Don’t start to extend payments to suppliers - at the end the end the customer is paying.

•

Especially key-vendors are essential. If those vendors stop to deliver, you are unable to produce anything.

•

Reminders for late payment, evil calls or bad credit-worthiness are the consequences.

•

Among troubles, what costs also time and money, you will enter into a risk to get worse conditions for existing and new vendors and certainly

also banks.

Instead

•

Prioritize verndors and segregate them for todays and future deliveries as well as for financial processes.

•

Rate your vendors individually, i.e. for readiness for deliver, quality of the deliveries, financial health, conditions. How vendors can be ratet is

part of our article in our news-corner here as an example for banks..

•

At least yearly negotiations with vendors. Time for personal meetings are well invested, instead just simple letters like: “beginning with next

month, we pay your invoices 4 days later”.

Read also our article about vendor management here.

B) Inventory

Don’t

•

Reduction of a safety stock can cost much more as it seems to be on a paper.

•

The consequences start with higher delivery costs, because a lower stock increase the number of orders per cycle. Higher prices arise in the

following because of scale-effects and also potential dissatisfaction of customers need to be considered because they don’t get their products

in the right time.

•

Impacts on turnover based incentives for the sales staff and the management may lead to troubles up to resignation and dismissals.

Instead

•

Deversify between semi-finished goods and finished goods. Semi-finished goods have an impact to the producution and have therefore just

indirect impact to the satisfaction of customers. Finished goods have an ultimate direct impact to the customers and therefore to the turnover.

•

Distinguish for goods with high, middle and low inventory turnover.

•

All goods should be compared by supplier in a matrix and clustered for the ideal lot size. See also our excel tool to calculate the ideal lot-size

by Andler for free download in our download area.

C) Customers

Don’t

•

Don’t dictate from one day to the other new payment terms. In the best case the customers ignore the new terms, but then nothing is

achieved. In the worst case customers quit the friendship.

•

Every customer is individual. Thus, don’t measure all customers with the same objectves.

•

Don’t think that customers stay because the product might a good one.

•

Don’t assume that a customer stays always the same.

Instead

•

Differentiate large and small customers as well as good and poor payer.

•

Have an interest for the customers of your customer in order to find out what those 2nd line customers request and how they behave. Thereby

you have a good basis for individual negotiations. Afterwards you are in a much better position to discuss more favourite payment and

delivery terms.

•

Be consequent with bad payer. Urge them max. twice and go then further with legal actions. Because it is much wiser to waive turnover as to

spend the products for nothing! Just alone with turnover on nice sheets nobody can pay their liabilities. That’s also the reason why turnover is

quite a bad kpi for incentives.

Read more about Working Capital in our article “Working Capital as Barometer of Effencieny”.

Contact us, we would be glad to show you the possible opportunities!

financial health. A positive working capital means that a company is theoretically

able to pay the shortterm liabilities. Nevertheless, with the requirement that

sufficient liquidity is available. Negative working capital means the respective

opposite.

Short Term Assets - Short Term Liabilities = Working Capital

(whereas short-term means with a remaining maturity of less than a year)

Terms, Key Performance Indicators

•

Days Sales Outstanding (DSO): Difference in days between invoice date and customer payment

•

Days Payable Outstanding (DPO): Difference in days between supplier invoice date and payment to supplier

•

Days Inventory Outstanding (DIO): Difference in days between invoice date of the supplier and the invoice to the customer for a specific good.

(Because the cash impact is not counting with the physical entry- or exit of the good in the warehouse. It is the invoice date of the supplier

invoice resp. invoice to the customer -> be aware of accruals!)

•

Days Working Capital (DWC) - Days, how long it needs to convert working capital in revenue. Also called “Cash Days”.

Calculation

1.

Direct Method: DSO - DPO + DIO = DWC

2.

Indirect Method: (WC[t2] - WC[t2] x 365 ) / Yearly Turnover = DWC

Example

With an assumed capital cost ratio of 8% the kpi’s of working capital

have these results:

DSO: 34'800.-

DIO: 6'666.67

DPO: -12'000.-

That equeals total costs of 29’466.67. Depending on further

circumstances these costs have also a direct impat to the liquidity.

The triggers for an optimization or trade receivables, trade payables

and mainly inventory turnover. For a sustainable success it is

mandatory to act strategic. That means, not just begging customers

for faster paymen or vendors for later payment. More from inside to

outside and thinking in clusters. Just this way a winning achievement

is possible. Are you interested how much your working capital cost and how much funds are locked? You will be surprised! Click here, in the

download area is a free excel tool to calculate those numbers.

Key Elements for Working Capital Management

•

Improvement of working capital unlocks frozen liquid funds, increase the free cash flow and reduce the inventory- and capital costs. (n.b. Free

Cash Flow = [Operating Cash Flow] + [Investment Cash Flow])

•

Consciously improvement of working capital processes release in average 20% - 30% tight capital.

•

The value of the company increase by re-investing the released funds. In consqueence the turnover rise what will lead to a better operational

cash flow by sametime reducing capital costs (same conditions assumed)

•

Working Capital is also an indicator for an upcoming crisis. If working capital rise faster than the turnover it means that more capital must have

been used that is at the end of the day just locked in operational processes. About three years before a liquidity crisis the ratio of [WC] /

[Balance Sheet Total] increase clearly.

Managing Working Capital

Working Capital is per definition the short term part of a general ledger (see above). But it will be managed also by long term driven positions. Short

Term: operational processes (Purchase, Sales, Payments). Long Term: liquidity effective procedures like the disposal of fixed assets for cash or

repayment of long term liabilities and also change in equity for capital fund.

Approach for Improvment

A) Vendors

Don’t

•

Don’t start to extend payments to suppliers - at the end the end the customer is paying.

•

Especially key-vendors are essential. If those vendors stop to deliver, you are unable to produce anything.

•

Reminders for late payment, evil calls or bad credit-worthiness are the consequences.

•

Among troubles, what costs also time and money, you will enter into a risk to get worse conditions for existing and new vendors and certainly

also banks.

Instead

•

Prioritize verndors and segregate them for todays and future deliveries as well as for financial processes.

•

Rate your vendors individually, i.e. for readiness for deliver, quality of the deliveries, financial health, conditions. How vendors can be ratet is

part of our article in our news-corner here as an example for banks..

•

At least yearly negotiations with vendors. Time for personal meetings are well invested, instead just simple letters like: “beginning with next

month, we pay your invoices 4 days later”.

Read also our article about vendor management here.

B) Inventory

Don’t

•

Reduction of a safety stock can cost much more as it seems to be on a paper.

•

The consequences start with higher delivery costs, because a lower stock increase the number of orders per cycle. Higher prices arise in the

following because of scale-effects and also potential dissatisfaction of customers need to be considered because they don’t get their products

in the right time.

•

Impacts on turnover based incentives for the sales staff and the management may lead to troubles up to resignation and dismissals.

Instead

•

Deversify between semi-finished goods and finished goods. Semi-finished goods have an impact to the producution and have therefore just

indirect impact to the satisfaction of customers. Finished goods have an ultimate direct impact to the customers and therefore to the turnover.

•

Distinguish for goods with high, middle and low inventory turnover.

•

All goods should be compared by supplier in a matrix and clustered for the ideal lot size. See also our excel tool to calculate the ideal lot-size

by Andler for free download in our download area.

C) Customers

Don’t

•

Don’t dictate from one day to the other new payment terms. In the best case the customers ignore the new terms, but then nothing is

achieved. In the worst case customers quit the friendship.

•

Every customer is individual. Thus, don’t measure all customers with the same objectves.

•

Don’t think that customers stay because the product might a good one.

•

Don’t assume that a customer stays always the same.

Instead

•

Differentiate large and small customers as well as good and poor payer.

•

Have an interest for the customers of your customer in order to find out what those 2nd line customers request and how they behave. Thereby

you have a good basis for individual negotiations. Afterwards you are in a much better position to discuss more favourite payment and

delivery terms.

•

Be consequent with bad payer. Urge them max. twice and go then further with legal actions. Because it is much wiser to waive turnover as to

spend the products for nothing! Just alone with turnover on nice sheets nobody can pay their liabilities. That’s also the reason why turnover is

quite a bad kpi for incentives.

Read more about Working Capital in our article “Working Capital as Barometer of Effencieny”.

Contact us, we would be glad to show you the possible opportunities!

financial health. A positive working capital means that a company is theoretically

able to pay the shortterm liabilities. Nevertheless, with the requirement that

sufficient liquidity is available. Negative working capital means the respective

opposite.

Short Term Assets - Short Term Liabilities = Working Capital

(whereas short-term means with a remaining maturity of less than a year)

Terms, Key Performance Indicators

•

Days Sales Outstanding (DSO): Difference in days between invoice date and customer payment

•

Days Payable Outstanding (DPO): Difference in days between supplier invoice date and payment to supplier

•

Days Inventory Outstanding (DIO): Difference in days between invoice date of the supplier and the invoice to the customer for a specific good.

(Because the cash impact is not counting with the physical entry- or exit of the good in the warehouse. It is the invoice date of the supplier

invoice resp. invoice to the customer -> be aware of accruals!)

•

Days Working Capital (DWC) - Days, how long it needs to convert working capital in revenue. Also called “Cash Days”.

Calculation

1.

Direct Method: DSO - DPO + DIO = DWC

2.

Indirect Method: (WC[t2] - WC[t2] x 365 ) / Yearly Turnover = DWC

Example

With an assumed capital cost ratio of 8% the kpi’s of working capital

have these results:

DSO: 34'800.-

DIO: 6'666.67

DPO: -12'000.-

That equeals total costs of 29’466.67. Depending on further

circumstances these costs have also a direct impat to the liquidity.

The triggers for an optimization or trade receivables, trade payables

and mainly inventory turnover. For a sustainable success it is

mandatory to act strategic. That means, not just begging customers

for faster paymen or vendors for later payment. More from inside to

outside and thinking in clusters. Just this way a winning achievement

is possible. Are you interested how much your working capital cost and how much funds are locked? You will be surprised! Click here, in the

download area is a free excel tool to calculate those numbers.

Key Elements for Working Capital Management

•

Improvement of working capital unlocks frozen liquid funds, increase the free cash flow and reduce the inventory- and capital costs. (n.b. Free

Cash Flow = [Operating Cash Flow] + [Investment Cash Flow])

•

Consciously improvement of working capital processes release in average 20% - 30% tight capital.

•

The value of the company increase by re-investing the released funds. In consqueence the turnover rise what will lead to a better operational

cash flow by sametime reducing capital costs (same conditions assumed)

•

Working Capital is also an indicator for an upcoming crisis. If working capital rise faster than the turnover it means that more capital must have

been used that is at the end of the day just locked in operational processes. About three years before a liquidity crisis the ratio of [WC] /

[Balance Sheet Total] increase clearly.

Managing Working Capital

Working Capital is per definition the short term part of a general ledger (see above). But it will be managed also by long term driven positions. Short

Term: operational processes (Purchase, Sales, Payments). Long Term: liquidity effective procedures like the disposal of fixed assets for cash or

repayment of long term liabilities and also change in equity for capital fund.

Approach for Improvment

A) Vendors

Don’t

•

Don’t start to extend payments to suppliers - at the end the end the customer is paying.

•

Especially key-vendors are essential. If those vendors stop to deliver, you are unable to produce anything.

•

Reminders for late payment, evil calls or bad credit-worthiness are the consequences.

•

Among troubles, what costs also time and money, you will enter into a risk to get worse conditions for existing and new vendors and certainly

also banks.

Instead

•

Prioritize verndors and segregate them for todays and future deliveries as well as for financial processes.

•

Rate your vendors individually, i.e. for readiness for deliver, quality of the deliveries, financial health, conditions. How vendors can be ratet is

part of our article in our news-corner here as an example for banks..

•

At least yearly negotiations with vendors. Time for personal meetings are well invested, instead just simple letters like: “beginning with next

month, we pay your invoices 4 days later”.

Read also our article about vendor management here.

B) Inventory

Don’t

•

Reduction of a safety stock can cost much more as it seems to be on a paper.

•

The consequences start with higher delivery costs, because a lower stock increase the number of orders per cycle. Higher prices arise in the

following because of scale-effects and also potential dissatisfaction of customers need to be considered because they don’t get their products

in the right time.

•

Impacts on turnover based incentives for the sales staff and the management may lead to troubles up to resignation and dismissals.

Instead

•

Deversify between semi-finished goods and finished goods. Semi-finished goods have an impact to the producution and have therefore just

indirect impact to the satisfaction of customers. Finished goods have an ultimate direct impact to the customers and therefore to the turnover.

•

Distinguish for goods with high, middle and low inventory turnover.

•

All goods should be compared by supplier in a matrix and clustered for the ideal lot size. See also our excel tool to calculate the ideal lot-size

by Andler for free download in our download area.

C) Customers

Don’t

•

Don’t dictate from one day to the other new payment terms. In the best case the customers ignore the new terms, but then nothing is

achieved. In the worst case customers quit the friendship.

•

Every customer is individual. Thus, don’t measure all customers with the same objectves.

•

Don’t think that customers stay because the product might a good one.

•

Don’t assume that a customer stays always the same.

Instead

•

Differentiate large and small customers as well as good and poor payer.

•

Have an interest for the customers of your customer in order to find out what those 2nd line customers request and how they behave. Thereby

you have a good basis for individual negotiations. Afterwards you are in a much better position to discuss more favourite payment and

delivery terms.

•

Be consequent with bad payer. Urge them max. twice and go then further with legal actions. Because it is much wiser to waive turnover as to

spend the products for nothing! Just alone with turnover on nice sheets nobody can pay their liabilities. That’s also the reason why turnover is

quite a bad kpi for incentives.

Read more about Working Capital in our article “Working Capital as Barometer of Effencieny”.

Contact us, we would be glad to show you the possible opportunities!

Working Capital / Tied Capital

Leaning of working capital processes reduce interest expenses,

release capital and improve key figures!

Working Capital may be defined by

efficiency of a company and their

shortterm financial health. A

positive working capital means that

a company is theoretically able to

pay the shortterm liabilities.

Nevertheless, with the requirement

that sufficient liquidity is available.

Negative working capital means the

respective opposite.

Short Term Assets - Short Term Liabilities = Working Capital

(whereas short-term means with a remaining maturity of less than a

year)

Terms, Key Performance Indicators

•

Days Sales Outstanding (DSO): Difference in days between

invoice date and customer payment

•

Days Payable Outstanding (DPO): Difference in days between

supplier invoice date and payment to supplier

•

Days Inventory Outstanding (DIO): Difference in days between

invoice date of the supplier and the invoice to the customer for

a specific good. (Because the cash impact is not counting with

the physical entry- or exit of the good in the warehouse. It is

the invoice date of the supplier invoice resp. invoice to the

customer -> be aware of accruals!)

•

Days Working Capital (DWC) - Days, how long it needs to

convert working capital in revenue. Also called “Cash Days”.

Calculation

1.

Direct Method: DSO - DPO + DIO = DWC

2.

Indirect Method: (WC[t2] - WC[t2] x 365 ) / Yearly Turnover =

DWC

Example

With an assumed capital cost ratio of 8% the kpi’s of working capital

have these results:

DSO: 34'800.-

DIO: 6'666.67

DPO: -12'000.-

That equeals total costs of 29’466.67. Depending on further

circumstances these costs have also a direct impat to the liquidity.

The triggers for an optimization or trade receivables, trade payables

and mainly inventory turnover. For a sustainable success it is

mandatory to act strategic. That means, not just begging customers

for faster paymen or vendors for later payment. More from inside to

outside and thinking in clusters. Just this way a winning achievement

is possible. Are you interested how much your working capital

cost and how much funds are locked? You will be surprised!

Click here, in the download area is a free excel tool to calculate

those numbers.

Key Elements for Working Capital Management

•

Improvement of working capital unlocks frozen liquid funds,

increase the free cash flow and reduce the inventory- and

capital costs. (n.b. Free Cash Flow = [Operating Cash Flow] +

[Investment Cash Flow])

•

Consciously improvement of working capital processes

release in average 20% - 30% tight capital.

•

The value of the company increase by re-investing the

released funds. In consqueence the turnover rise what will

lead to a better operational cash flow by sametime reducing

capital costs (same conditions assumed)

•

Working Capital is also an indicator for an upcoming crisis. If

working capital rise faster than the turnover it means that more

capital must have been used that is at the end of the day just

locked in operational processes. About three years before a

liquidity crisis the ratio of [WC] / [Balance Sheet Total]

increase clearly.

Managing Working Capital

Working Capital is per definition the short term part of a general

ledger (see above). But it will be managed also by long term driven

positions. Short Term: operational processes (Purchase, Sales,

Payments). Long Term: liquidity effective procedures like the

disposal of fixed assets for cash or repayment of long term liabilities

and also change in equity for capital fund.

Approach for Improvment

A) Vendors

Don’t

•

Don’t start to extend payments to suppliers - at the end the

end the customer is paying.

•

Especially key-vendors are essential. If those vendors stop to

deliver, you are unable to produce anything.

•

Reminders for late payment, evil calls or bad credit-worthiness

are the consequences.

•

Among troubles, what costs also time and money, you will

enter into a risk to get worse conditions for existing and new

vendors and certainly also banks.

Instead

•

Prioritize verndors and segregate them for todays and future

deliveries as well as for financial processes.

•

Rate your vendors individually, i.e. for readiness for deliver,

quality of the deliveries, financial health, conditions. How

vendors can be ratet is part of our article in our news-corner

here as an example for banks..

•

At least yearly negotiations with vendors. Time for personal

meetings are well invested, instead just simple letters like:

“beginning with next month, we pay your invoices 4 days

later”.

Read also our article about vendor management here.

B) Inventory

Don’t

•

Reduction of a safety stock can cost much more as it seems to

be on a paper.

•

The consequences start with higher delivery costs, because a

lower stock increase the number of orders per cycle. Higher

prices arise in the following because of scale-effects and also

potential dissatisfaction of customers need to be considered

because they don’t get their products in the right time.

•

Impacts on turnover based incentives for the sales staff and

the management may lead to troubles up to resignation and

dismissals.

Instead

•

Deversify between semi-finished goods and finished goods.

Semi-finished goods have an impact to the producution and

have therefore just indirect impact to the satisfaction of

customers. Finished goods have an ultimate direct impact to

the customers and therefore to the turnover.

•

Distinguish for goods with high, middle and low inventory

turnover.

•

All goods should be compared by supplier in a matrix and

clustered for the ideal lot size. See also our excel tool to

calculate the ideal lot-size by Andler for free download in our

download area.

C) Customers

Don’t

•

Don’t dictate from one day to the other new payment terms. In

the best case the customers ignore the new terms, but then

nothing is achieved. In the worst case customers quit the

friendship.

•

Every customer is individual. Thus, don’t measure all

customers with the same objectves.

•

Don’t think that customers stay because the product might a

good one.

•

Don’t assume that a customer stays always the same.

Instead

•

Differentiate large and small customers as well as good and

poor payer.

•

Have an interest for the customers of your customer in order to

find out what those 2nd line customers request and how they

behave. Thereby you have a good basis for individual

negotiations. Afterwards you are in a much better position to

discuss more favourite payment and delivery terms.

•

Be consequent with bad payer. Urge them max. twice and go

then further with legal actions. Because it is much wiser to

waive turnover as to spend the products for nothing! Just

alone with turnover on nice sheets nobody can pay their

liabilities. That’s also the reason why turnover is quite a bad

kpi for incentives.

Read more about Working Capital in our article “Working

Capital as Barometer of Effencieny”.

Contact us, we would be glad to show you the possible

opportunities!

efficiency of a company and their

shortterm financial health. A

positive working capital means that

a company is theoretically able to

pay the shortterm liabilities.

Nevertheless, with the requirement

that sufficient liquidity is available.

Negative working capital means the

respective opposite.

Short Term Assets - Short Term Liabilities = Working Capital

(whereas short-term means with a remaining maturity of less than a

year)

Terms, Key Performance Indicators

•

Days Sales Outstanding (DSO): Difference in days between

invoice date and customer payment

•

Days Payable Outstanding (DPO): Difference in days between

supplier invoice date and payment to supplier

•

Days Inventory Outstanding (DIO): Difference in days between

invoice date of the supplier and the invoice to the customer for

a specific good. (Because the cash impact is not counting with

the physical entry- or exit of the good in the warehouse. It is

the invoice date of the supplier invoice resp. invoice to the

customer -> be aware of accruals!)

•

Days Working Capital (DWC) - Days, how long it needs to

convert working capital in revenue. Also called “Cash Days”.

Calculation

1.

Direct Method: DSO - DPO + DIO = DWC

2.

Indirect Method: (WC[t2] - WC[t2] x 365 ) / Yearly Turnover =

DWC

Example

With an assumed capital cost ratio of 8% the kpi’s of working capital

have these results:

DSO: 34'800.-

DIO: 6'666.67

DPO: -12'000.-

That equeals total costs of 29’466.67. Depending on further

circumstances these costs have also a direct impat to the liquidity.

The triggers for an optimization or trade receivables, trade payables

and mainly inventory turnover. For a sustainable success it is

mandatory to act strategic. That means, not just begging customers

for faster paymen or vendors for later payment. More from inside to

outside and thinking in clusters. Just this way a winning achievement

is possible. Are you interested how much your working capital

cost and how much funds are locked? You will be surprised!

Click here, in the download area is a free excel tool to calculate

those numbers.

Key Elements for Working Capital Management

•

Improvement of working capital unlocks frozen liquid funds,

increase the free cash flow and reduce the inventory- and

capital costs. (n.b. Free Cash Flow = [Operating Cash Flow] +

[Investment Cash Flow])

•

Consciously improvement of working capital processes

release in average 20% - 30% tight capital.

•

The value of the company increase by re-investing the

released funds. In consqueence the turnover rise what will

lead to a better operational cash flow by sametime reducing

capital costs (same conditions assumed)

•

Working Capital is also an indicator for an upcoming crisis. If

working capital rise faster than the turnover it means that more

capital must have been used that is at the end of the day just

locked in operational processes. About three years before a

liquidity crisis the ratio of [WC] / [Balance Sheet Total]

increase clearly.

Managing Working Capital

Working Capital is per definition the short term part of a general

ledger (see above). But it will be managed also by long term driven

positions. Short Term: operational processes (Purchase, Sales,

Payments). Long Term: liquidity effective procedures like the

disposal of fixed assets for cash or repayment of long term liabilities

and also change in equity for capital fund.

Approach for Improvment

A) Vendors

Don’t

•

Don’t start to extend payments to suppliers - at the end the

end the customer is paying.

•

Especially key-vendors are essential. If those vendors stop to

deliver, you are unable to produce anything.

•

Reminders for late payment, evil calls or bad credit-worthiness

are the consequences.

•

Among troubles, what costs also time and money, you will

enter into a risk to get worse conditions for existing and new

vendors and certainly also banks.

Instead

•

Prioritize verndors and segregate them for todays and future

deliveries as well as for financial processes.

•

Rate your vendors individually, i.e. for readiness for deliver,

quality of the deliveries, financial health, conditions. How

vendors can be ratet is part of our article in our news-corner

here as an example for banks..

•

At least yearly negotiations with vendors. Time for personal

meetings are well invested, instead just simple letters like:

“beginning with next month, we pay your invoices 4 days

later”.

Read also our article about vendor management here.

B) Inventory

Don’t

•

Reduction of a safety stock can cost much more as it seems to

be on a paper.

•

The consequences start with higher delivery costs, because a

lower stock increase the number of orders per cycle. Higher

prices arise in the following because of scale-effects and also

potential dissatisfaction of customers need to be considered

because they don’t get their products in the right time.

•

Impacts on turnover based incentives for the sales staff and

the management may lead to troubles up to resignation and

dismissals.

Instead

•

Deversify between semi-finished goods and finished goods.

Semi-finished goods have an impact to the producution and

have therefore just indirect impact to the satisfaction of

customers. Finished goods have an ultimate direct impact to

the customers and therefore to the turnover.

•

Distinguish for goods with high, middle and low inventory

turnover.

•

All goods should be compared by supplier in a matrix and

clustered for the ideal lot size. See also our excel tool to

calculate the ideal lot-size by Andler for free download in our

download area.

C) Customers

Don’t

•

Don’t dictate from one day to the other new payment terms. In

the best case the customers ignore the new terms, but then

nothing is achieved. In the worst case customers quit the

friendship.

•

Every customer is individual. Thus, don’t measure all

customers with the same objectves.

•

Don’t think that customers stay because the product might a

good one.

•

Don’t assume that a customer stays always the same.

Instead

•

Differentiate large and small customers as well as good and

poor payer.

•

Have an interest for the customers of your customer in order to

find out what those 2nd line customers request and how they

behave. Thereby you have a good basis for individual

negotiations. Afterwards you are in a much better position to

discuss more favourite payment and delivery terms.

•

Be consequent with bad payer. Urge them max. twice and go

then further with legal actions. Because it is much wiser to

waive turnover as to spend the products for nothing! Just

alone with turnover on nice sheets nobody can pay their

liabilities. That’s also the reason why turnover is quite a bad

kpi for incentives.

Read more about Working Capital in our article “Working

Capital as Barometer of Effencieny”.

Contact us, we would be glad to show you the possible

opportunities!