Currency Overlay

How think and act Big-Players when hedging their

Share-, Currency-, Commodity- and Interest Risk?

In general, the exchange of amounts in different currencies is a zero-sum game. The reason that some participants of the foreign exchange market manage their foreign currency positions actively make it to some of them possible to operate above the zero-border. Thus, to the

burden of other participants.

The Market

The prospect of the foreign exchange market has changed increasingly in recent years. It is no longer considered as a minor product of

international trading- and capital markets, it is now also respected as a form of investment. Funds- and Hedge Fund Manager, whose strategies

often don't meet the expectations because of low volatility in the equity markets, decided to create foreign exchange strategies and startet to

build their own currency funds. Funds are going increasingly more sophisticated in the use of currency vehicles in order to increase their gains.

At least it will be tempted so, because the predictability is nearly impossible, because there are myriad of paramers which couldn't be sufficient

calculated, e.g. human logic.

The Participants

A look into the publications of the funds shows it: there is no doubt about that the number of Funds investing into

currencies is having more and more popularity. On the contrary most Asset Managers, Treasurer and Cash

Manager deal with currencies for a transactional background, i.e. underlying. That means, behind a trade is in

most cases a "real" transaction with goods or fixed assets, e.g. shares. So far no pure aim for profit, just rather a

hedge or a simple change from one currency to another currency, because it is needed physically today or in the

future. The behaviour for improvement is reduced to the negotiation of better prices regarding the change.

Smaller customers do it by phone, middle customers by their Treasury Management System and larger customers

with special broker-software which is online with multiple banks. The best bank-offer gets the deal.

The decission of the Bank resp. the Institutional Market Participant

It can be discussed about the benefits of such software. On the one side it is just simply easy to calculate the profit threshold for the market

participant, i.e. the customer. On the other hand there is the question about the timing. Should the order now at 11:00:00, at 11:00:10 or at

11:01:00 executed and where is then the rate? This coincidence factor cannot be calculated and the band within a minute in the foreign

exchange market can be huge, relatively seen to the tough negotiations for one or two pips only.

The Winner and the Loser

About one thing all market participants agree: currency risk is always present, as long

as it is not naturally hedged (e.g. assets vs. capital, revenues vs. expenses in the same

currency at the same time). This risk must be recognized and managed. Banks offer to

especially institutional customers, thereof mainly from the volumes perspective the

funds with their enormous resources, tailored resp. structured products in order to have

the currency exposure under control at lowest possible costs. But the principle of a zero-

sum game is still present. The questions arise, who are the losers in that global trading

system. At the end of the day all of us in the one or other form. May it be by direct

losses, non-taken gains, higher margins on the products which we trade or consume

daily. Therefore the global circle is going to be closed. Nevertheless, every market

participant is trying for his own benefit to get his best possible optimum. This leads to

the question where this optimum can be fixed and how high the tolerance for losses is for each single participant?

Pension Funds which do not manage their currency exposure proactive and therefore don't hedge, expose themselves clear and take into

account the gains and losses occurred by exchange rate. Hence, it exists on the one hand a financing matter and on the other hand a portfolio

efficiency question. If Enterprises and Pension Funds take this risk just into account it can be derived the assumption that those risks are

managed separately in another asset class in order to get back in the "save" profit zone. Most of the Companies and Funds drive on a strategy

in the middle. That means, hedge currency exposure partially and additionally the volatility from price differences occurred by currency

exchange effects.

With the attempt to save the earnings and to expand them, pension funds continuously increase the part of shares denominated in foreign

currencies. Doing this, they increase their currency exposure. That in combination with the active management of investment vehicle is the

main reason for the expandation of the professional category of the Cash Manager. In former times those tasks have been managed

outsourced to specialized companies, but in line with the always more upcoming internationalization the currency exchange risk is also

increasing. Unification of currencies, like the Euro, are the absolute exception to reduce that risk.

Get the Optimum, regardless what the intention of the Market Participant is

It must be distinguished between

1. Trading, Production and Service Enterprises (the companies) and

2. Institutional Investors.

The first group attempt, as already mentioned above, minimizing their risk while the second group try to

generate gains with those risks. But both have one and the same consensus: get the optimum out

of the currency market.

Currency Overlay

In a strategic and tactical investment process, FX can be a separate asset class and currency exposure can reduce expected portfolio risk.

Active currency overlay positions are in general uncorrelated with bond and equity positions. A successful active FX management increases the

portfolio return and should be viewed as a natural part in a fund's alpha process.

Our Partner, Mercury Control AG, Switzerland, applies a strictly disciplined style rotation strategy, based on continuous macro, political and flow

analysis across the G7 currencies and are combined with technical forecasting tools. The trading style itself is selected from the following

options, accordingly:

•

Momentum

•

Range

•

Volatility

Momentung Trading

Momentum Trading acts as the overarching style, inasmuch as it determines trade execution according to a principal outlook for mid- to long-

term movements governing the FX market. Its role is also to set the stage for Range Trading - the most commonly applied FX trading style - by

identifying the maximum and minimum range lines to execute trades, according to risk-return principles.

Range Trading

Range Trading, on the other hand, analyzes the underlying channeling patterns (range) resulting from currently prevailing "paid price"

scenarios. The clear goal is to trade as long as possible within such a range in order to maximize the value-adding potential of this style .

Volatility (Vega) Trading

A final rotation to Volatility Trading occurs when a previously applied range "breaks out" to either side and no clear continuation is immediately

detectable. As a result, options are written on the existing short (sold) or long (bought) positions. However, once all Volatility Trading

possibilities are exhausted there is a logical movement back to Momentum or Range Trading.

The risk or hedge ratio between 0% and 100% and the base currency specified by the client defines the proportional amount of the mandate's

absolute currency exposure. This means, either an active or a passive managed mandate.

Active currency management enables the client to reduce risk and add return to an international portfolio whereas the passive

approach negates the foreign exchange risk and reduces the diversification benefits from international investments

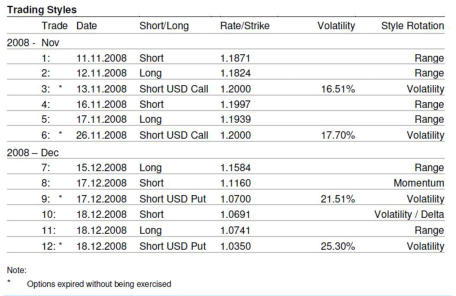

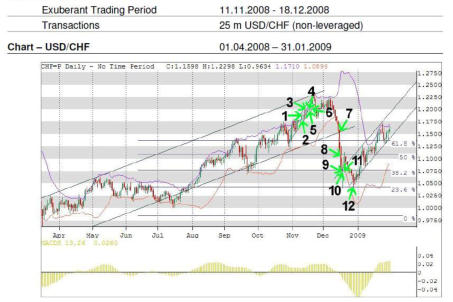

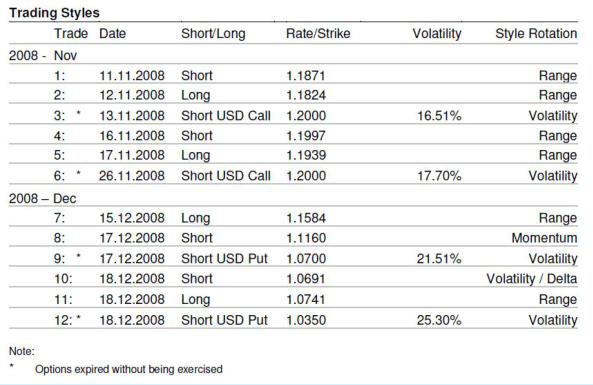

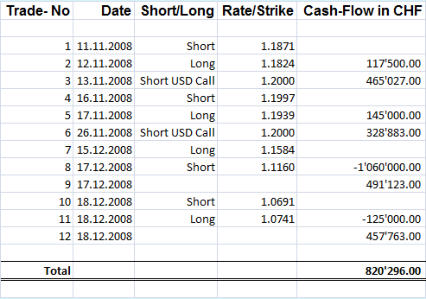

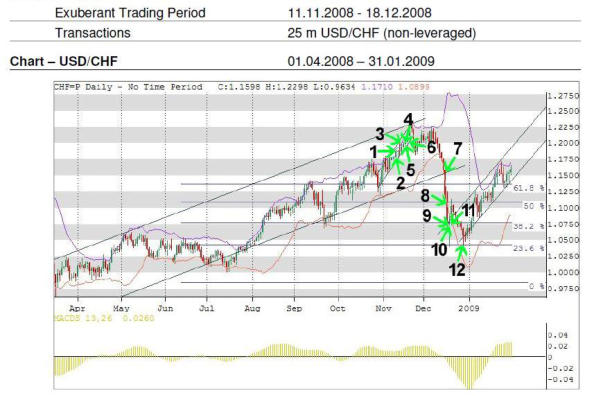

Case Study

The following is a case study for a customer:

Related Cash Flows to above mentioned trades:

In other words, a Treasurer with functional currency CHF and need of reducing FX-exposure for $ 7.2m is now able to compensate his loss of

long USD 7.2m x (1.0741-1.1871)= - CHF 813’600 with the gain of the overlay transactions whereas a Treasurer or Fund-Manager with need

of opimizing his $ 25m investment achieved an annualized gross-profit of 28,2%.

Hint: in case of using Currency Overlay for hedging purpose, we recommend according best practice risk management to apply a value at risk

approach in order to adjust the overlay portfolio to the current underlying and complete it with an absolute loss amount.

Do you like to know more about Currency Overlay? Don’t hesitate and contact us.

market manage their foreign currency positions actively make it to some of them possible to operate above the zero-border. Thus, to the

burden of other participants.

The Market

The prospect of the foreign exchange market has changed increasingly in recent years. It is no longer considered as a minor product of

international trading- and capital markets, it is now also respected as a form of investment. Funds- and Hedge Fund Manager, whose strategies

often don't meet the expectations because of low volatility in the equity markets, decided to create foreign exchange strategies and startet to

build their own currency funds. Funds are going increasingly more sophisticated in the use of currency vehicles in order to increase their gains.

At least it will be tempted so, because the predictability is nearly impossible, because there are myriad of paramers which couldn't be sufficient

calculated, e.g. human logic.

The Participants

A look into the publications of the funds shows it: there is no doubt about that the number of Funds investing into

currencies is having more and more popularity. On the contrary most Asset Managers, Treasurer and Cash

Manager deal with currencies for a transactional background, i.e. underlying. That means, behind a trade is in

most cases a "real" transaction with goods or fixed assets, e.g. shares. So far no pure aim for profit, just rather a

hedge or a simple change from one currency to another currency, because it is needed physically today or in the

future. The behaviour for improvement is reduced to the negotiation of better prices regarding the change.

Smaller customers do it by phone, middle customers by their Treasury Management System and larger customers

with special broker-software which is online with multiple banks. The best bank-offer gets the deal.

The decission of the Bank resp. the Institutional Market Participant

It can be discussed about the benefits of such software. On the one side it is just simply easy to calculate the profit threshold for the market

participant, i.e. the customer. On the other hand there is the question about the timing. Should the order now at 11:00:00, at 11:00:10 or at

11:01:00 executed and where is then the rate? This coincidence factor cannot be calculated and the band within a minute in the foreign

exchange market can be huge, relatively seen to the tough negotiations for one or two pips only.

The Winner and the Loser

About one thing all market participants agree: currency risk is always present, as long

as it is not naturally hedged (e.g. assets vs. capital, revenues vs. expenses in the same

currency at the same time). This risk must be recognized and managed. Banks offer to

especially institutional customers, thereof mainly from the volumes perspective the

funds with their enormous resources, tailored resp. structured products in order to have

the currency exposure under control at lowest possible costs. But the principle of a zero-

sum game is still present. The questions arise, who are the losers in that global trading

system. At the end of the day all of us in the one or other form. May it be by direct

losses, non-taken gains, higher margins on the products which we trade or consume

daily. Therefore the global circle is going to be closed. Nevertheless, every market

participant is trying for his own benefit to get his best possible optimum. This leads to

the question where this optimum can be fixed and how high the tolerance for losses is for each single participant?

Pension Funds which do not manage their currency exposure proactive and therefore don't hedge, expose themselves clear and take into

account the gains and losses occurred by exchange rate. Hence, it exists on the one hand a financing matter and on the other hand a portfolio

efficiency question. If Enterprises and Pension Funds take this risk just into account it can be derived the assumption that those risks are

managed separately in another asset class in order to get back in the "save" profit zone. Most of the Companies and Funds drive on a strategy

in the middle. That means, hedge currency exposure partially and additionally the volatility from price differences occurred by currency

exchange effects.

With the attempt to save the earnings and to expand them, pension funds continuously increase the part of shares denominated in foreign

currencies. Doing this, they increase their currency exposure. That in combination with the active management of investment vehicle is the

main reason for the expandation of the professional category of the Cash Manager. In former times those tasks have been managed

outsourced to specialized companies, but in line with the always more upcoming internationalization the currency exchange risk is also

increasing. Unification of currencies, like the Euro, are the absolute exception to reduce that risk.

Get the Optimum, regardless what the intention of the Market Participant is

It must be distinguished between

1. Trading, Production and Service Enterprises (the companies) and

2. Institutional Investors.

The first group attempt, as already mentioned above, minimizing their risk while the second group try to

generate gains with those risks. But both have one and the same consensus: get the optimum out

of the currency market.

Currency Overlay

In a strategic and tactical investment process, FX can be a separate asset class and currency exposure can reduce expected portfolio risk.

Active currency overlay positions are in general uncorrelated with bond and equity positions. A successful active FX management increases the

portfolio return and should be viewed as a natural part in a fund's alpha process.

Our Partner, Mercury Control AG, Switzerland, applies a strictly disciplined style rotation strategy, based on continuous macro, political and flow

analysis across the G7 currencies and are combined with technical forecasting tools. The trading style itself is selected from the following

options, accordingly:

•

Momentum

•

Range

•

Volatility

Momentung Trading

Momentum Trading acts as the overarching style, inasmuch as it determines trade execution according to a principal outlook for mid- to long-

term movements governing the FX market. Its role is also to set the stage for Range Trading - the most commonly applied FX trading style - by

identifying the maximum and minimum range lines to execute trades, according to risk-return principles.

Range Trading

Range Trading, on the other hand, analyzes the underlying channeling patterns (range) resulting from currently prevailing "paid price"

scenarios. The clear goal is to trade as long as possible within such a range in order to maximize the value-adding potential of this style .

Volatility (Vega) Trading

A final rotation to Volatility Trading occurs when a previously applied range "breaks out" to either side and no clear continuation is immediately

detectable. As a result, options are written on the existing short (sold) or long (bought) positions. However, once all Volatility Trading

possibilities are exhausted there is a logical movement back to Momentum or Range Trading.

The risk or hedge ratio between 0% and 100% and the base currency specified by the client defines the proportional amount of the mandate's

absolute currency exposure. This means, either an active or a passive managed mandate.

Active currency management enables the client to reduce risk and add return to an international portfolio whereas the passive

approach negates the foreign exchange risk and reduces the diversification benefits from international investments

Case Study

The following is a case study for a customer:

Related Cash Flows to above mentioned trades:

In other words, a Treasurer with functional currency CHF and need of reducing FX-exposure for $ 7.2m is now able to compensate his loss of

long USD 7.2m x (1.0741-1.1871)= - CHF 813’600 with the gain of the overlay transactions whereas a Treasurer or Fund-Manager with need

of opimizing his $ 25m investment achieved an annualized gross-profit of 28,2%.

Hint: in case of using Currency Overlay for hedging purpose, we recommend according best practice risk management to apply a value at risk

approach in order to adjust the overlay portfolio to the current underlying and complete it with an absolute loss amount.

Do you like to know more about Currency Overlay? Don’t hesitate and contact us.

market manage their foreign currency positions actively make it to some of them possible to operate above the zero-border. Thus, to the

burden of other participants.

The Market

The prospect of the foreign exchange market has changed increasingly in recent years. It is no longer considered as a minor product of

international trading- and capital markets, it is now also respected as a form of investment. Funds- and Hedge Fund Manager, whose strategies

often don't meet the expectations because of low volatility in the equity markets, decided to create foreign exchange strategies and startet to

build their own currency funds. Funds are going increasingly more sophisticated in the use of currency vehicles in order to increase their gains.

At least it will be tempted so, because the predictability is nearly impossible, because there are myriad of paramers which couldn't be sufficient

calculated, e.g. human logic.

The Participants

A look into the publications of the funds shows it: there is no doubt about that the number of Funds investing into

currencies is having more and more popularity. On the contrary most Asset Managers, Treasurer and Cash

Manager deal with currencies for a transactional background, i.e. underlying. That means, behind a trade is in

most cases a "real" transaction with goods or fixed assets, e.g. shares. So far no pure aim for profit, just rather a

hedge or a simple change from one currency to another currency, because it is needed physically today or in the

future. The behaviour for improvement is reduced to the negotiation of better prices regarding the change.

Smaller customers do it by phone, middle customers by their Treasury Management System and larger customers

with special broker-software which is online with multiple banks. The best bank-offer gets the deal.

The decission of the Bank resp. the Institutional Market Participant

It can be discussed about the benefits of such software. On the one side it is just simply easy to calculate the profit threshold for the market

participant, i.e. the customer. On the other hand there is the question about the timing. Should the order now at 11:00:00, at 11:00:10 or at

11:01:00 executed and where is then the rate? This coincidence factor cannot be calculated and the band within a minute in the foreign

exchange market can be huge, relatively seen to the tough negotiations for one or two pips only.

The Winner and the Loser

About one thing all market participants agree: currency risk is always present, as long

as it is not naturally hedged (e.g. assets vs. capital, revenues vs. expenses in the same

currency at the same time). This risk must be recognized and managed. Banks offer to

especially institutional customers, thereof mainly from the volumes perspective the

funds with their enormous resources, tailored resp. structured products in order to have

the currency exposure under control at lowest possible costs. But the principle of a zero-

sum game is still present. The questions arise, who are the losers in that global trading

system. At the end of the day all of us in the one or other form. May it be by direct

losses, non-taken gains, higher margins on the products which we trade or consume

daily. Therefore the global circle is going to be closed. Nevertheless, every market

participant is trying for his own benefit to get his best possible optimum. This leads to

the question where this optimum can be fixed and how high the tolerance for losses is for each single participant?

Pension Funds which do not manage their currency exposure proactive and therefore don't hedge, expose themselves clear and take into

account the gains and losses occurred by exchange rate. Hence, it exists on the one hand a financing matter and on the other hand a portfolio

efficiency question. If Enterprises and Pension Funds take this risk just into account it can be derived the assumption that those risks are

managed separately in another asset class in order to get back in the "save" profit zone. Most of the Companies and Funds drive on a strategy

in the middle. That means, hedge currency exposure partially and additionally the volatility from price differences occurred by currency

exchange effects.

With the attempt to save the earnings and to expand them, pension funds continuously increase the part of shares denominated in foreign

currencies. Doing this, they increase their currency exposure. That in combination with the active management of investment vehicle is the

main reason for the expandation of the professional category of the Cash Manager. In former times those tasks have been managed

outsourced to specialized companies, but in line with the always more upcoming internationalization the currency exchange risk is also

increasing. Unification of currencies, like the Euro, are the absolute exception to reduce that risk.

Get the Optimum, regardless what the intention of the Market Participant is

It must be distinguished between

1. Trading, Production and Service Enterprises (the companies) and

2. Institutional Investors.

The first group attempt, as already mentioned above, minimizing their risk while the second group try to

generate gains with those risks. But both have one and the same consensus: get the optimum out

of the currency market.

Currency Overlay

In a strategic and tactical investment process, FX can be a separate asset class and currency exposure can reduce expected portfolio risk.

Active currency overlay positions are in general uncorrelated with bond and equity positions. A successful active FX management increases the

portfolio return and should be viewed as a natural part in a fund's alpha process.

Our Partner, Mercury Control AG, Switzerland, applies a strictly disciplined style rotation strategy, based on continuous macro, political and flow

analysis across the G7 currencies and are combined with technical forecasting tools. The trading style itself is selected from the following

options, accordingly:

•

Momentum

•

Range

•

Volatility

Momentung Trading

Momentum Trading acts as the overarching style, inasmuch as it determines trade execution according to a principal outlook for mid- to long-

term movements governing the FX market. Its role is also to set the stage for Range Trading - the most commonly applied FX trading style - by

identifying the maximum and minimum range lines to execute trades, according to risk-return principles.

Range Trading

Range Trading, on the other hand, analyzes the underlying channeling patterns (range) resulting from currently prevailing "paid price"

scenarios. The clear goal is to trade as long as possible within such a range in order to maximize the value-adding potential of this style .

Volatility (Vega) Trading

A final rotation to Volatility Trading occurs when a previously applied range "breaks out" to either side and no clear continuation is immediately

detectable. As a result, options are written on the existing short (sold) or long (bought) positions. However, once all Volatility Trading

possibilities are exhausted there is a logical movement back to Momentum or Range Trading.

The risk or hedge ratio between 0% and 100% and the base currency specified by the client defines the proportional amount of the mandate's

absolute currency exposure. This means, either an active or a passive managed mandate.

Active currency management enables the client to reduce risk and add return to an international portfolio whereas the passive

approach negates the foreign exchange risk and reduces the diversification benefits from international investments

Case Study

The following is a case study for a customer:

Related Cash Flows to above mentioned trades:

In other words, a Treasurer with functional currency CHF and need of reducing FX-exposure for $ 7.2m is now able to compensate his loss of

long USD 7.2m x (1.0741-1.1871)= - CHF 813’600 with the gain of the overlay transactions whereas a Treasurer or Fund-Manager with need

of opimizing his $ 25m investment achieved an annualized gross-profit of 28,2%.

Hint: in case of using Currency Overlay for hedging purpose, we recommend according best practice risk management to apply a value at risk

approach in order to adjust the overlay portfolio to the current underlying and complete it with an absolute loss amount.

Do you like to know more about Currency Overlay? Don’t hesitate and contact us.

Currency Overlay

How think and act Big-Players when hedging their

Share-, Currency-, Commodity- and Interest Risk?

In general, the exchange of amounts in different currencies is a zero-

sum game. The reason that some participants of the foreign

exchange market manage their foreign currency positions actively

make it to some of them possible to operate above the zero-border.

Thus, to the burden of other participants.

The Market

The prospect of the foreign exchange market has changed

increasingly in recent years. It is no longer considered as a minor

product of international trading- and capital markets, it is now also

respected as a form of investment. Funds- and Hedge Fund

Manager, whose strategies often don't meet the expectations

because of low volatility in the equity markets, decided to create

foreign exchange strategies and startet to build their own currency

funds. Funds are going increasingly more sophisticated in the use of

currency vehicles in order to increase their gains. At least it will be

tempted so, because the predictability is nearly impossible, because

there are myriad of paramers which couldn't be sufficient calculated,

e.g. human logic.

The Participants

A look into the publications of the

funds shows it: there is no doubt

about that the number of Funds

investing into currencies is having

more and more popularity. On the

contrary most Asset Managers,

Treasurer and Cash Manager deal

with currencies for a transactional

background, i.e. underlying. That

means, behind a trade is in most

cases a "real" transaction with goods or fixed assets, e.g. shares. So

far no pure aim for profit, just rather a hedge or a simple change

from one currency to another currency, because it is needed

physically today or in the future. The behaviour for improvement is

reduced to the negotiation of better prices regarding the change.

Smaller customers do it by phone, middle customers by their

Treasury Management System and larger customers with special

broker-software which is online with multiple banks. The best bank-

offer gets the deal.

The decission of the Bank resp. the Institutional Market

Participant

It can be discussed about the benefits of such software. On the one

side it is just simply easy to calculate the profit threshold for the

market participant, i.e. the customer. On the other hand there is the

question about the timing. Should the order now at 11:00:00, at

11:00:10 or at 11:01:00 executed and where is then the rate? This

coincidence factor cannot be calculated and the band within a

minute in the foreign exchange market can be huge, relatively seen

to the tough negotiations for one or two pips only.

The Winner and the Loser

About one thing all market participants agree: currency risk is always

present, as long as it is not naturally hedged (e.g. assets vs. capital,

revenues vs. expenses in the same currency at the same time). This

risk must be recognized and managed. Banks offer to especially

institutional customers, thereof mainly from the volumes perspective

the funds with their enormous resources, tailored resp. structured

products in order to have the currency exposure under control at

lowest possible costs. But the principle of a zero-sum game is still

present. The questions arise, who are the losers in that global

trading system. At the end of the day all of us in the one or other

form. May it be by direct losses, non-taken gains, higher margins on

the products which we trade or consume daily. Therefore the global

circle is going to be closed. Nevertheless, every market participant is

trying for his own benefit to get his best possible optimum. This

leads to the question where this optimum can be fixed and how high

the tolerance for losses is for each single participant?

Pension Funds which do not manage their currency exposure

proactive and therefore don't hedge, expose themselves clear and

take into account the gains and losses occurred by exchange rate.

Hence, it exists on the one hand a financing matter and on the other

hand a portfolio efficiency question. If Enterprises and Pension

Funds take this risk just into account it can be derived the

assumption that those risks are managed separately in another

asset class in order to get back in the "save" profit zone. Most of the

Companies and Funds drive on a strategy in the middle. That

means, hedge currency exposure partially and additionally the

volatility from price differences occurred by currency exchange

effects.

With the attempt to save the earnings and to expand them, pension

funds continuously increase the part of shares denominated in

foreign currencies. Doing this, they increase their currency

exposure. That in combination with the active management of

investment vehicle is the main reason for the expandation of the

professional category of the Cash Manager. In former times those

tasks have been managed outsourced to specialized companies, but

in line with the always more upcoming internationalization the

currency exchange risk is also increasing. Unification of currencies,

like the Euro, are the absolute exception to reduce that risk.

Get the Optimum, regardless what the intention of the

Market Participant is

It must be distinguished

between

1. Trading, Production and

Service Enterprises (the

companies) and

2. Institutional Investors.

The first group attempt, as already mentioned above, minimizing

their risk while the second group try to generate gains with those

risks. But both have one and the same consensus: get the

optimum out of the currency market.

Currency Overlay

In a strategic and tactical investment process, FX can be a separate

asset class and currency exposure can reduce expected portfolio

risk. Active currency overlay positions are in general uncorrelated

with bond and equity positions. A successful active FX management

increases the portfolio return and should be viewed as a natural part

in a fund's alpha process.

Our Partner, Mercury Control AG, Switzerland, applies a strictly

disciplined style rotation strategy, based on continuous macro,

political and flow analysis across the G7 currencies and are

combined with technical forecasting tools. The trading style itself is

selected from the following options, accordingly:

•

Momentum

•

Range

•

Volatility

Momentung Trading

Momentum Trading acts as the overarching style, inasmuch as it

determines trade execution according to a principal outlook for mid-

to long-term movements governing the FX market. Its role is also to

set the stage for Range Trading - the most commonly applied FX

trading style - by identifying the maximum and minimum range lines

to execute trades, according to risk-return principles.

Range Trading

Range Trading, on the other hand, analyzes the underlying

channeling patterns (range) resulting from currently prevailing "paid

price" scenarios. The clear goal is to trade as long as possible within

such a range in order to maximize the value-adding potential of this

style .

Volatility (Vega) Trading

A final rotation to Volatility Trading occurs when a previously applied

range "breaks out" to either side and no clear continuation is

immediately detectable. As a result, options are written on the

existing short (sold) or long (bought) positions. However, once all

Volatility Trading possibilities are exhausted there is a logical

movement back to Momentum or Range Trading.

The risk or hedge ratio between 0% and 100% and the base

currency specified by the client defines the proportional amount of

the mandate's absolute currency exposure. This means, either an

active or a passive managed mandate.

Active currency management enables the client to reduce

risk and add return to an international portfolio whereas the

passive approach negates the foreign exchange risk and

reduces the diversification benefits from international

investments

Case Study

The following is a case study for a customer:

Related Cash Flows to above mentioned trades:

In other words, a Treasurer with functional currency CHF and need

of reducing FX-exposure for $ 7.2m is now able to compensate his

loss of long USD 7.2m x (1.0741-1.1871)= - CHF 813’600 with the

gain of the overlay transactions whereas a Treasurer or Fund-

Manager with need of opimizing his $ 25m investment achieved an

annualized gross-profit of 28,2%.

Hint: in case of using Currency Overlay for hedging purpose, we

recommend according best practice risk management to apply a

value at risk approach in order to adjust the overlay portfolio to the

current underlying and complete it with an absolute loss amount.

Do you like to know more about Currency Overlay?

Don’t hesitate and contact us.

exchange market manage their foreign currency positions actively

make it to some of them possible to operate above the zero-border.

Thus, to the burden of other participants.

The Market

The prospect of the foreign exchange market has changed

increasingly in recent years. It is no longer considered as a minor

product of international trading- and capital markets, it is now also

respected as a form of investment. Funds- and Hedge Fund

Manager, whose strategies often don't meet the expectations

because of low volatility in the equity markets, decided to create

foreign exchange strategies and startet to build their own currency

funds. Funds are going increasingly more sophisticated in the use of

currency vehicles in order to increase their gains. At least it will be

tempted so, because the predictability is nearly impossible, because

there are myriad of paramers which couldn't be sufficient calculated,

e.g. human logic.

The Participants

A look into the publications of the

funds shows it: there is no doubt

about that the number of Funds

investing into currencies is having

more and more popularity. On the

contrary most Asset Managers,

Treasurer and Cash Manager deal

with currencies for a transactional

background, i.e. underlying. That

means, behind a trade is in most

cases a "real" transaction with goods or fixed assets, e.g. shares. So

far no pure aim for profit, just rather a hedge or a simple change

from one currency to another currency, because it is needed

physically today or in the future. The behaviour for improvement is

reduced to the negotiation of better prices regarding the change.

Smaller customers do it by phone, middle customers by their

Treasury Management System and larger customers with special

broker-software which is online with multiple banks. The best bank-

offer gets the deal.

The decission of the Bank resp. the Institutional Market

Participant

It can be discussed about the benefits of such software. On the one

side it is just simply easy to calculate the profit threshold for the

market participant, i.e. the customer. On the other hand there is the

question about the timing. Should the order now at 11:00:00, at

11:00:10 or at 11:01:00 executed and where is then the rate? This

coincidence factor cannot be calculated and the band within a

minute in the foreign exchange market can be huge, relatively seen

to the tough negotiations for one or two pips only.

The Winner and the Loser

About one thing all market participants agree: currency risk is always

present, as long as it is not naturally hedged (e.g. assets vs. capital,

revenues vs. expenses in the same currency at the same time). This

risk must be recognized and managed. Banks offer to especially

institutional customers, thereof mainly from the volumes perspective

the funds with their enormous resources, tailored resp. structured

products in order to have the currency exposure under control at

lowest possible costs. But the principle of a zero-sum game is still

present. The questions arise, who are the losers in that global

trading system. At the end of the day all of us in the one or other

form. May it be by direct losses, non-taken gains, higher margins on

the products which we trade or consume daily. Therefore the global

circle is going to be closed. Nevertheless, every market participant is

trying for his own benefit to get his best possible optimum. This

leads to the question where this optimum can be fixed and how high

the tolerance for losses is for each single participant?

Pension Funds which do not manage their currency exposure

proactive and therefore don't hedge, expose themselves clear and

take into account the gains and losses occurred by exchange rate.

Hence, it exists on the one hand a financing matter and on the other

hand a portfolio efficiency question. If Enterprises and Pension

Funds take this risk just into account it can be derived the

assumption that those risks are managed separately in another

asset class in order to get back in the "save" profit zone. Most of the

Companies and Funds drive on a strategy in the middle. That

means, hedge currency exposure partially and additionally the

volatility from price differences occurred by currency exchange

effects.

With the attempt to save the earnings and to expand them, pension

funds continuously increase the part of shares denominated in

foreign currencies. Doing this, they increase their currency

exposure. That in combination with the active management of

investment vehicle is the main reason for the expandation of the

professional category of the Cash Manager. In former times those

tasks have been managed outsourced to specialized companies, but

in line with the always more upcoming internationalization the

currency exchange risk is also increasing. Unification of currencies,

like the Euro, are the absolute exception to reduce that risk.

Get the Optimum, regardless what the intention of the

Market Participant is

It must be distinguished

between

1. Trading, Production and

Service Enterprises (the

companies) and

2. Institutional Investors.

The first group attempt, as already mentioned above, minimizing

their risk while the second group try to generate gains with those

risks. But both have one and the same consensus: get the

optimum out of the currency market.

Currency Overlay

In a strategic and tactical investment process, FX can be a separate

asset class and currency exposure can reduce expected portfolio

risk. Active currency overlay positions are in general uncorrelated

with bond and equity positions. A successful active FX management

increases the portfolio return and should be viewed as a natural part

in a fund's alpha process.

Our Partner, Mercury Control AG, Switzerland, applies a strictly

disciplined style rotation strategy, based on continuous macro,

political and flow analysis across the G7 currencies and are

combined with technical forecasting tools. The trading style itself is

selected from the following options, accordingly:

•

Momentum

•

Range

•

Volatility

Momentung Trading

Momentum Trading acts as the overarching style, inasmuch as it

determines trade execution according to a principal outlook for mid-

to long-term movements governing the FX market. Its role is also to

set the stage for Range Trading - the most commonly applied FX

trading style - by identifying the maximum and minimum range lines

to execute trades, according to risk-return principles.

Range Trading

Range Trading, on the other hand, analyzes the underlying

channeling patterns (range) resulting from currently prevailing "paid

price" scenarios. The clear goal is to trade as long as possible within

such a range in order to maximize the value-adding potential of this

style .

Volatility (Vega) Trading

A final rotation to Volatility Trading occurs when a previously applied

range "breaks out" to either side and no clear continuation is

immediately detectable. As a result, options are written on the

existing short (sold) or long (bought) positions. However, once all

Volatility Trading possibilities are exhausted there is a logical

movement back to Momentum or Range Trading.

The risk or hedge ratio between 0% and 100% and the base

currency specified by the client defines the proportional amount of

the mandate's absolute currency exposure. This means, either an

active or a passive managed mandate.

Active currency management enables the client to reduce

risk and add return to an international portfolio whereas the

passive approach negates the foreign exchange risk and

reduces the diversification benefits from international

investments

Case Study

The following is a case study for a customer:

Related Cash Flows to above mentioned trades:

In other words, a Treasurer with functional currency CHF and need

of reducing FX-exposure for $ 7.2m is now able to compensate his

loss of long USD 7.2m x (1.0741-1.1871)= - CHF 813’600 with the

gain of the overlay transactions whereas a Treasurer or Fund-

Manager with need of opimizing his $ 25m investment achieved an

annualized gross-profit of 28,2%.

Hint: in case of using Currency Overlay for hedging purpose, we

recommend according best practice risk management to apply a

value at risk approach in order to adjust the overlay portfolio to the

current underlying and complete it with an absolute loss amount.

Do you like to know more about Currency Overlay?

Don’t hesitate and contact us.