Group / Intercompany Netting

Do you have multiple subsidiaries with intercompany payments?

Do they pay the IC-invoices to each other direct? -

This bears high risks, is inefficient and cost a lot of money!

Netting, derived from the action "to net" is a process in which receivables and payables are compared to each other for all group companies and cleared, i.e. settled vs. each other through a centralized Netting Center - also called Corporated Netting Center. Final reason is the payment

(mostly, but not always in cash), reduced to just one amount which is paid / received only. But the largest benefits are not visible at a first glance!

Provided that at this point netting in organisational terms is only intended for for receivables and payabels occurred within a legal group

structure: the clearing of accounts receivables- and payables is also common practice, but ends with the single vendor-customer relationship.

However, the principle idea is the same.

Way of posing a Problem / Task

Meet this example also your group?

•

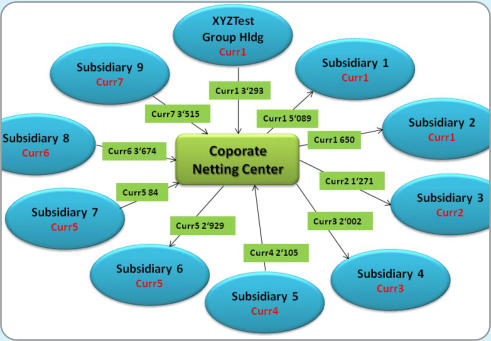

XYZTest Group, holding in country A with subsidiaries (controlled) in countries A, B, C, D, E and F.

•

A delivers to B and E and invoicesin currency A.

•

C delivers to A and D and invoices in currency C.

•

D delivers to E and invoices in currenc E.

•

etc etc.

Therefore following problems arised and in relation to it, these risks will arise:

A) Quantitative Impact

1.

High expenses for payment orders because of a large number of payment transactions.

2.

Foreign exchange risk at the receiver of the rendered service. Those are often in other countries and/or receivables in other currencies

than the one they need to settle the invoice. Conclusion: due to internal process external risks are build up! They can be measured

quantitative for example with Value at Risk resp. Cash Flow at Risk.

3.

Foreign Exchange costs: for the same reason as 2. above the reciever of the service has to pay relative quite low amounts. Often

dedited/credited from an account, which is denominated in another currency than the invoice-currency. These additional transaction costs

are approx. 2%-4% of the total invoice amount! In these days, where margins have to be calculated on the second digit after the comma

and agreed in heavy negotiationes, this way of paying invoices can be considered as pure destruction of money.

4.

With every single payment also the risk increase of manual input errors that it will be paid too much or too less. This leads to binding of

intensive human resource power what is at the end expensive. If you would measure these items for a specific period the one and other

CFO would wonder what he pays for this unfavourable process.

5.

In case the foreign exchange risk would be centralized by a netting process, the netting center would be able a) to eliminate these fx-risk

in a first step (overlay) and b) to manage the remaining amount per currency with hedging, for instance fx-swaps.

B) Qualitative Impact

1.

The counterparty risk increase with every single transaction. Imagine, you give your bank a payment order and your bank has no direct

nostro account with the correspoding bank of the beneficiary. Such payment processes through intermediary banks are very common in

the international payment system. Assume that the intermediary bank is Lehman Brothers. You as ordering party don’t know that and have

no control about it. But in case of a total shortfall of this intermediary bank you have to pay this total loss! Because this risk is

just hardly to be quantified we mention it here as qualitative risk.

2.

Monthly and quarterly intercompany reconciliation is unpopular, time consuming, fraught with risks and therefore need to be implicitely

avoided. A centralized reconciliation which is always up to date can be outweight in these times with gold. Due to the permanent clearing

process, the typical monthly- and quarterly differences will be (if they still happen) resolved in very short time. And: not by the Accountant

which is heavy under pressure during closing days, new by a Treasury Manager which has anyway the overview about all transactions

throughout the month.

Concerned Transactions

The characteristic of the concerned transactions is given by the legal frame: receivables and payments need to be due and in their content need

to be qualified for netting. Most intercompany transactions are:

•

Local expenes which have been pre-paid by a entity

•

Interest from intercompany loans

•

Products from a pre-production (e.g. unfinished goods)

•

Management Fee

•

Service Fee

•

Corp. Re-Charges with fix determined key

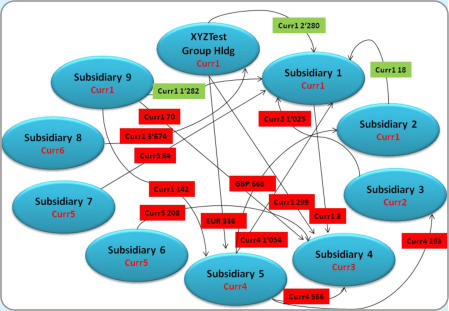

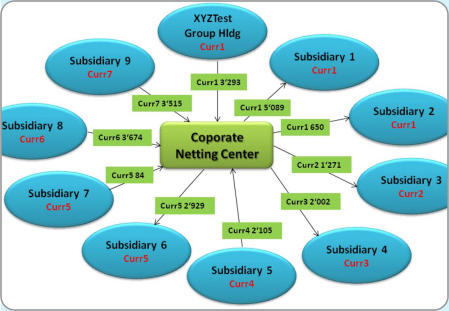

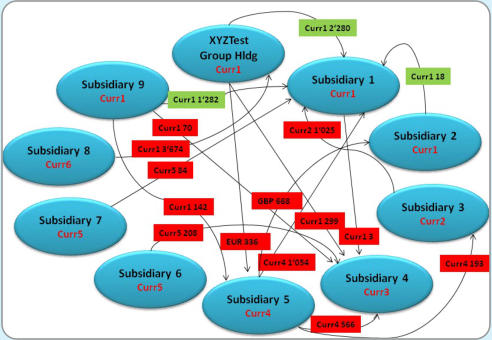

From Chaos to Order

A) Before

B) After

Organization

As monitored in the “After” picture above, the Corporate Netting Center is the central key-element between all group companies. Hence, the

question for the location of the corporate netting center is already given.

Preferrably the Netting Center should a) belong to the Treasury Department and b) at a location which should qualify for possible tax benefits

because of double tax agreements and as less as possible restrictions by local authorities. Those are complicate and often discretionary by the

responsible officials. Positive examples are the Netherlands, Luxembourg (under the consideration that both have to apply European Untion

law), Switzerland and especially Singapore. Negative examples are all countries in Africa, Russia, most of the Latin American coutnries,

especially Venezuela and Argentina.

Risks

Nothing in our world is without risk and nothing is for free (Adam Smith mention it already in his Wealth of Nations). Starting with the

implementation risk that current processes are going to be changed can be a risk. With exact- and important, professional planning as well as

balancing strenghts - weakness - chances in a project those risks are recognized and can be held under control. In order of completeness we

mention at this point the risk of transfer pricing, which, also recognized in time, is then no more risk.

Summary

By introducing a central clearing center, called Corporate Netting Center, many expensive costs are avoided with less complexetiy (mostly in

relation to IT-investments which are very low with our Treasury Software STS, valuable risks are reduced and reconciliation processes are made

clearly more simple . Order now a free presentation for managing Group Netting and see here how it works.

Contact us, we would be glad to show you the possible opportunities!

cleared, i.e. settled vs. each other through a centralized Netting Center - also called Corporated Netting Center. Final reason is the payment

(mostly, but not always in cash), reduced to just one amount which is paid / received only. But the largest benefits are not visible at a first glance!

Provided that at this point netting in organisational terms is only intended for for receivables and payabels occurred within a legal group

structure: the clearing of accounts receivables- and payables is also common practice, but ends with the single vendor-customer relationship.

However, the principle idea is the same.

Way of posing a Problem / Task

Meet this example also your group?

•

XYZTest Group, holding in country A with subsidiaries (controlled) in countries A, B, C, D, E and F.

•

A delivers to B and E and invoicesin currency A.

•

C delivers to A and D and invoices in currency C.

•

D delivers to E and invoices in currenc E.

•

etc etc.

Therefore following problems arised and in relation to it, these risks will arise:

A) Quantitative Impact

1.

High expenses for payment orders because of a large number of payment transactions.

2.

Foreign exchange risk at the receiver of the rendered service. Those are often in other countries and/or receivables in other currencies

than the one they need to settle the invoice. Conclusion: due to internal process external risks are build up! They can be measured

quantitative for example with Value at Risk resp. Cash Flow at Risk.

3.

Foreign Exchange costs: for the same reason as 2. above the reciever of the service has to pay relative quite low amounts. Often

dedited/credited from an account, which is denominated in another currency than the invoice-currency. These additional transaction costs

are approx. 2%-4% of the total invoice amount! In these days, where margins have to be calculated on the second digit after the comma

and agreed in heavy negotiationes, this way of paying invoices can be considered as pure destruction of money.

4.

With every single payment also the risk increase of manual input errors that it will be paid too much or too less. This leads to binding of

intensive human resource power what is at the end expensive. If you would measure these items for a specific period the one and other

CFO would wonder what he pays for this unfavourable process.

5.

In case the foreign exchange risk would be centralized by a netting process, the netting center would be able a) to eliminate these fx-risk

in a first step (overlay) and b) to manage the remaining amount per currency with hedging, for instance fx-swaps.

B) Qualitative Impact

1.

The counterparty risk increase with every single transaction. Imagine, you give your bank a payment order and your bank has no direct

nostro account with the correspoding bank of the beneficiary. Such payment processes through intermediary banks are very common in

the international payment system. Assume that the intermediary bank is Lehman Brothers. You as ordering party don’t know that and have

no control about it. But in case of a total shortfall of this intermediary bank you have to pay this total loss! Because this risk is

just hardly to be quantified we mention it here as qualitative risk.

2.

Monthly and quarterly intercompany reconciliation is unpopular, time consuming, fraught with risks and therefore need to be implicitely

avoided. A centralized reconciliation which is always up to date can be outweight in these times with gold. Due to the permanent clearing

process, the typical monthly- and quarterly differences will be (if they still happen) resolved in very short time. And: not by the Accountant

which is heavy under pressure during closing days, new by a Treasury Manager which has anyway the overview about all transactions

throughout the month.

Concerned Transactions

The characteristic of the concerned transactions is given by the legal frame: receivables and payments need to be due and in their content need

to be qualified for netting. Most intercompany transactions are:

•

Local expenes which have been pre-paid by a entity

•

Interest from intercompany loans

•

Products from a pre-production (e.g. unfinished goods)

•

Management Fee

•

Service Fee

•

Corp. Re-Charges with fix determined key

From Chaos to Order

A) Before

B) After

Organization

As monitored in the “After” picture above, the Corporate Netting Center is the central key-element between all group companies. Hence, the

question for the location of the corporate netting center is already given.

Preferrably the Netting Center should a) belong to the Treasury Department and b) at a location which should qualify for possible tax benefits

because of double tax agreements and as less as possible restrictions by local authorities. Those are complicate and often discretionary by the

responsible officials. Positive examples are the Netherlands, Luxembourg (under the consideration that both have to apply European Untion

law), Switzerland and especially Singapore. Negative examples are all countries in Africa, Russia, most of the Latin American coutnries,

especially Venezuela and Argentina.

Risks

Nothing in our world is without risk and nothing is for free (Adam Smith mention it already in his Wealth of Nations). Starting with the

implementation risk that current processes are going to be changed can be a risk. With exact- and important, professional planning as well as

balancing strenghts - weakness - chances in a project those risks are recognized and can be held under control. In order of completeness we

mention at this point the risk of transfer pricing, which, also recognized in time, is then no more risk.

Summary

By introducing a central clearing center, called Corporate Netting Center, many expensive costs are avoided with less complexetiy (mostly in

relation to IT-investments which are very low with our Treasury Software STS, valuable risks are reduced and reconciliation processes are made

clearly more simple . Order now a free presentation for managing Group Netting and see here how it works.

Contact us, we would be glad to show you the possible opportunities!

cleared, i.e. settled vs. each other through a centralized Netting Center - also called Corporated Netting Center. Final reason is the payment

(mostly, but not always in cash), reduced to just one amount which is paid / received only. But the largest benefits are not visible at a first glance!

Provided that at this point netting in organisational terms is only intended for for receivables and payabels occurred within a legal group

structure: the clearing of accounts receivables- and payables is also common practice, but ends with the single vendor-customer relationship.

However, the principle idea is the same.

Way of posing a Problem / Task

Meet this example also your group?

•

XYZTest Group, holding in country A with subsidiaries (controlled) in countries A, B, C, D, E and F.

•

A delivers to B and E and invoicesin currency A.

•

C delivers to A and D and invoices in currency C.

•

D delivers to E and invoices in currenc E.

•

etc etc.

Therefore following problems arised and in relation to it, these risks will arise:

A) Quantitative Impact

1.

High expenses for payment orders because of a large number of payment transactions.

2.

Foreign exchange risk at the receiver of the rendered service. Those are often in other countries and/or receivables in other currencies

than the one they need to settle the invoice. Conclusion: due to internal process external risks are build up! They can be measured

quantitative for example with Value at Risk resp. Cash Flow at Risk.

3.

Foreign Exchange costs: for the same reason as 2. above the reciever of the service has to pay relative quite low amounts. Often

dedited/credited from an account, which is denominated in another currency than the invoice-currency. These additional transaction costs

are approx. 2%-4% of the total invoice amount! In these days, where margins have to be calculated on the second digit after the comma

and agreed in heavy negotiationes, this way of paying invoices can be considered as pure destruction of money.

4.

With every single payment also the risk increase of manual input errors that it will be paid too much or too less. This leads to binding of

intensive human resource power what is at the end expensive. If you would measure these items for a specific period the one and other

CFO would wonder what he pays for this unfavourable process.

5.

In case the foreign exchange risk would be centralized by a netting process, the netting center would be able a) to eliminate these fx-risk

in a first step (overlay) and b) to manage the remaining amount per currency with hedging, for instance fx-swaps.

B) Qualitative Impact

1.

The counterparty risk increase with every single transaction. Imagine, you give your bank a payment order and your bank has no direct

nostro account with the correspoding bank of the beneficiary. Such payment processes through intermediary banks are very common in

the international payment system. Assume that the intermediary bank is Lehman Brothers. You as ordering party don’t know that and have

no control about it. But in case of a total shortfall of this intermediary bank you have to pay this total loss! Because this risk is

just hardly to be quantified we mention it here as qualitative risk.

2.

Monthly and quarterly intercompany reconciliation is unpopular, time consuming, fraught with risks and therefore need to be implicitely

avoided. A centralized reconciliation which is always up to date can be outweight in these times with gold. Due to the permanent clearing

process, the typical monthly- and quarterly differences will be (if they still happen) resolved in very short time. And: not by the Accountant

which is heavy under pressure during closing days, new by a Treasury Manager which has anyway the overview about all transactions

throughout the month.

Concerned Transactions

The characteristic of the concerned transactions is given by the legal frame: receivables and payments need to be due and in their content need

to be qualified for netting. Most intercompany transactions are:

•

Local expenes which have been pre-paid by a entity

•

Interest from intercompany loans

•

Products from a pre-production (e.g. unfinished goods)

•

Management Fee

•

Service Fee

•

Corp. Re-Charges with fix determined key

From Chaos to Order

A) Before

B) After

Organization

As monitored in the “After” picture above, the Corporate Netting Center is the central key-element between all group companies. Hence, the

question for the location of the corporate netting center is already given.

Preferrably the Netting Center should a) belong to the Treasury Department and b) at a location which should qualify for possible tax benefits

because of double tax agreements and as less as possible restrictions by local authorities. Those are complicate and often discretionary by the

responsible officials. Positive examples are the Netherlands, Luxembourg (under the consideration that both have to apply European Untion

law), Switzerland and especially Singapore. Negative examples are all countries in Africa, Russia, most of the Latin American coutnries,

especially Venezuela and Argentina.

Risks

Nothing in our world is without risk and nothing is for free (Adam Smith mention it already in his Wealth of Nations). Starting with the

implementation risk that current processes are going to be changed can be a risk. With exact- and important, professional planning as well as

balancing strenghts - weakness - chances in a project those risks are recognized and can be held under control. In order of completeness we

mention at this point the risk of transfer pricing, which, also recognized in time, is then no more risk.

Summary

By introducing a central clearing center, called Corporate Netting Center, many expensive costs are avoided with less complexetiy (mostly in

relation to IT-investments which are very low with our Treasury Software STS, valuable risks are reduced and reconciliation processes are made

clearly more simple . Order now a free presentation for managing Group Netting and see here how it works.

Contact us, we would be glad to show you the possible opportunities!

Group / Intercompany Netting

Do you have multiple subsidiaries with intercompany payments?

Do they pay the IC-invoices to each other direct? -

This bears high risks, is inefficient and cost a lot of money!

Netting, derived from the action "to net" is a process in which

receivables and payables are compared to each other for all group

companies and cleared, i.e. settled vs. each other through a

centralized Netting Center - also called Corporated Netting Center.

Final reason is the payment (mostly, but not always in cash),

reduced to just one amount which is paid / received only. But the

largest benefits are not visible at a first glance!

Provided that at this point netting in organisational terms is only

intended for for receivables and payabels occurred within a legal

group structure: the clearing of accounts receivables- and payables

is also common practice, but ends with the single vendor-customer

relationship. However, the principle idea is the same.

Way of posing a Problem / Task

Meet this example also your group?

•

XYZTest Group, holding in country A with subsidiaries

(controlled) in countries A, B, C, D, E and F.

•

A delivers to B and E and invoicesin currency A.

•

C delivers to A and D and invoices in currency C.

•

D delivers to E and invoices in currenc E.

•

etc etc.

Therefore following problems arised and in relation to it, these risks

will arise:

A) Quantitative Impact

1.

High expenses for payment orders because of a large number

of payment transactions.

2.

Foreign exchange risk at the receiver of the rendered service.

Those are often in other countries and/or receivables in other

currencies than the one they need to settle the invoice.

Conclusion: due to internal process external risks are

build up! They can be measured quantitative for example with

Value at Risk resp. Cash Flow at Risk.

3.

Foreign Exchange costs: for the same reason as 2. above the

reciever of the service has to pay relative quite low amounts.

Often dedited/credited from an account, which is denominated

in another currency than the invoice-currency. These additional

transaction costs are approx. 2%-4% of the total invoice

amount! In these days, where margins have to be calculated

on the second digit after the comma and agreed in heavy

negotiationes, this way of paying invoices can be considered

as pure destruction of money.

4.

With every single payment also the risk increase of manual

input errors that it will be paid too much or too less. This leads

to binding of intensive human resource power what is at the

end expensive. If you would measure these items for a specific

period the one and other CFO would wonder what he pays for

this unfavourable process.

5.

In case the foreign exchange risk would be centralized by a

netting process, the netting center would be able a) to

eliminate these fx-risk in a first step (overlay) and b) to

manage the remaining amount per currency with hedging, for

instance fx-swaps.

B) Qualitative Impact

1.

The counterparty risk increase with every single transaction.

Imagine, you give your bank a payment order and your bank

has no direct nostro account with the correspoding bank of the

beneficiary. Such payment processes through intermediary

banks are very common in the international payment system.

Assume that the intermediary bank is Lehman Brothers. You

as ordering party don’t know that and have no control about it.

But in case of a total shortfall of this intermediary bank

you have to pay this total loss! Because this risk is just

hardly to be quantified we mention it here as qualitative risk.

2.

Monthly and quarterly intercompany reconciliation is

unpopular, time consuming, fraught with risks and therefore

need to be implicitely avoided. A centralized reconciliation

which is always up to date can be outweight in these times

with gold. Due to the permanent clearing process, the typical

monthly- and quarterly differences will be (if they still happen)

resolved in very short time. And: not by the Accountant which

is heavy under pressure during closing days, new by a

Treasury Manager which has anyway the overview about all

transactions throughout the month.

Concerned Transactions

The characteristic of the concerned transactions is given by the legal

frame: receivables and payments need to be due and in their content

need to be qualified for netting. Most intercompany transactions are:

•

Local expenes which have been pre-paid by a entity

•

Interest from intercompany loans

•

Products from a pre-production (e.g. unfinished goods)

•

Management Fee

•

Service Fee

•

Corp. Re-Charges with fix determined key

From Chaos to Order

A) Before

B) Afterwards

Organization

As monitored in the “After” picture above, the Corporate Netting

Center is the central key-element between all group companies.

Hence, the question for the location of the corporate netting center is

already given.

Preferrably the Netting Center should a) belong to the Treasury

Department and b) at a location which should qualify for possible tax

benefits because of double tax agreements and as less as possible

restrictions by local authorities. Those are complicate and often

discretionary by the responsible officials. Positive examples are the

Netherlands, Luxembourg (under the consideration that both have to

apply European Untion law), Switzerland and especially Singapore.

Negative examples are all countries in Africa, Russia, most of the

Latin American coutnries, especially Venezuela and Argentina.

Risks

Nothing in our world is without risk and nothing is for free (Adam

Smith mention it already in his Wealth of Nations). Starting with the

implementation risk that current processes are going to be changed

can be a risk. With exact- and important, professional planning as

well as balancing strenghts - weakness - chances in a project those

risks are recognized and can be held under control. In order of

completeness we mention at this point the risk of transfer pricing,

which, also recognized in time, is then no more risk.

Summary

By introducing a central clearing center, called Corporate Netting

Center, many expensive costs are avoided with less complexetiy

(mostly in relation to IT-investments which are very low with our

Treasury Software STS, valuable risks are reduced and

reconciliation processes are made clearly more simple . Order now

a free presentation for managing Group Netting and see here

how it works.

Contact us, we would be glad to show you the possible

opportunities!

receivables and payables are compared to each other for all group

companies and cleared, i.e. settled vs. each other through a

centralized Netting Center - also called Corporated Netting Center.

Final reason is the payment (mostly, but not always in cash),

reduced to just one amount which is paid / received only. But the

largest benefits are not visible at a first glance!

Provided that at this point netting in organisational terms is only

intended for for receivables and payabels occurred within a legal

group structure: the clearing of accounts receivables- and payables

is also common practice, but ends with the single vendor-customer

relationship. However, the principle idea is the same.

Way of posing a Problem / Task

Meet this example also your group?

•

XYZTest Group, holding in country A with subsidiaries

(controlled) in countries A, B, C, D, E and F.

•

A delivers to B and E and invoicesin currency A.

•

C delivers to A and D and invoices in currency C.

•

D delivers to E and invoices in currenc E.

•

etc etc.

Therefore following problems arised and in relation to it, these risks

will arise:

A) Quantitative Impact

1.

High expenses for payment orders because of a large number

of payment transactions.

2.

Foreign exchange risk at the receiver of the rendered service.

Those are often in other countries and/or receivables in other

currencies than the one they need to settle the invoice.

Conclusion: due to internal process external risks are

build up! They can be measured quantitative for example with

Value at Risk resp. Cash Flow at Risk.

3.

Foreign Exchange costs: for the same reason as 2. above the

reciever of the service has to pay relative quite low amounts.

Often dedited/credited from an account, which is denominated

in another currency than the invoice-currency. These additional

transaction costs are approx. 2%-4% of the total invoice

amount! In these days, where margins have to be calculated

on the second digit after the comma and agreed in heavy

negotiationes, this way of paying invoices can be considered

as pure destruction of money.

4.

With every single payment also the risk increase of manual

input errors that it will be paid too much or too less. This leads

to binding of intensive human resource power what is at the

end expensive. If you would measure these items for a specific

period the one and other CFO would wonder what he pays for

this unfavourable process.

5.

In case the foreign exchange risk would be centralized by a

netting process, the netting center would be able a) to

eliminate these fx-risk in a first step (overlay) and b) to

manage the remaining amount per currency with hedging, for

instance fx-swaps.

B) Qualitative Impact

1.

The counterparty risk increase with every single transaction.

Imagine, you give your bank a payment order and your bank

has no direct nostro account with the correspoding bank of the

beneficiary. Such payment processes through intermediary

banks are very common in the international payment system.

Assume that the intermediary bank is Lehman Brothers. You

as ordering party don’t know that and have no control about it.

But in case of a total shortfall of this intermediary bank

you have to pay this total loss! Because this risk is just

hardly to be quantified we mention it here as qualitative risk.

2.

Monthly and quarterly intercompany reconciliation is

unpopular, time consuming, fraught with risks and therefore

need to be implicitely avoided. A centralized reconciliation

which is always up to date can be outweight in these times

with gold. Due to the permanent clearing process, the typical

monthly- and quarterly differences will be (if they still happen)

resolved in very short time. And: not by the Accountant which

is heavy under pressure during closing days, new by a

Treasury Manager which has anyway the overview about all

transactions throughout the month.

Concerned Transactions

The characteristic of the concerned transactions is given by the legal

frame: receivables and payments need to be due and in their content

need to be qualified for netting. Most intercompany transactions are:

•

Local expenes which have been pre-paid by a entity

•

Interest from intercompany loans

•

Products from a pre-production (e.g. unfinished goods)

•

Management Fee

•

Service Fee

•

Corp. Re-Charges with fix determined key

From Chaos to Order

A) Before

B) Afterwards

Organization

As monitored in the “After” picture above, the Corporate Netting

Center is the central key-element between all group companies.

Hence, the question for the location of the corporate netting center is

already given.

Preferrably the Netting Center should a) belong to the Treasury

Department and b) at a location which should qualify for possible tax

benefits because of double tax agreements and as less as possible

restrictions by local authorities. Those are complicate and often

discretionary by the responsible officials. Positive examples are the

Netherlands, Luxembourg (under the consideration that both have to

apply European Untion law), Switzerland and especially Singapore.

Negative examples are all countries in Africa, Russia, most of the

Latin American coutnries, especially Venezuela and Argentina.

Risks

Nothing in our world is without risk and nothing is for free (Adam

Smith mention it already in his Wealth of Nations). Starting with the

implementation risk that current processes are going to be changed

can be a risk. With exact- and important, professional planning as

well as balancing strenghts - weakness - chances in a project those

risks are recognized and can be held under control. In order of

completeness we mention at this point the risk of transfer pricing,

which, also recognized in time, is then no more risk.

Summary

By introducing a central clearing center, called Corporate Netting

Center, many expensive costs are avoided with less complexetiy

(mostly in relation to IT-investments which are very low with our

Treasury Software STS, valuable risks are reduced and

reconciliation processes are made clearly more simple . Order now

a free presentation for managing Group Netting and see here

how it works.

Contact us, we would be glad to show you the possible

opportunities!