Loans

Loans - that’s something everybody seems to know and understand.

Not necessarely! The practice often shows considerable comprehension questions.

Loans are considered generally often as fiddling, totally intelligible and more over, as a simple financial agreement. But in practice quite often comprehensive questions arise which lead sometimes to serious problems because of a lack of technical knowledge and/or legal

understandings.

Fundamentials

Technical

This small mindmap shows that a loan has many facings. Dependent, what the goal of a loans is, many different details should be

considered carefully:

Technical Questions

1.

Interest source, e.g. from a newspaper or not approved google hits instead of a common market source - e.g. LIBOR, EURIBOR etc.

2.

Interest calculation, e.g. because of the currency and duration the correct day-count coventions need to be applied.

3.

Fundamential calculations, e.g. a loan which started at 30.06.xx and ends at 31.12.xx with a prolongation to 30.06.yy is calculated

30.12.xx - 31.12.xx and 01.01.yy - 30.06.yy. Here, one day is missing, the day from 31.12.xx- 01.01.yy!

Legal Aspects

The following explanations refer to the greatest possible extend on commercial law from 1. World

countries, e.g. Middle-Europe, North-America. But dependent on the specific country there may be

clear differences in the local law!

The substantial characteristics of a (money)loan is the obligation of the lender to deliver to the

borrower a certain amount for a specific time by transfer of ownership (delivery-obligation) and the

borrower has the obligation to repay the amount at the end (re-payment obligation). Additionally it

is an essential attribute of the lender to leave the amount during the live-time of the loan at the

borrower (relinquish-obligation).

However, the interest is for a loan not necessarely to be defined, as exiting it may sound in the first moment. Because interest is not equal

the loan, it is a separate item, i.e. the compensation of the lender for the usage of capital (= loan) during a certain period of time. So, in

common affairs interest is just payable if they had been agreed. Basically. But: in most of the laws there is an additional clause which says

that in commercial business interest is payable also without a special agreement.

Interest has additionally fundamential legal characteristics: If an agreement for interest is missing, one may conclude that it is in fact not a

loan in common sense, hence a repayment of the loan is not an obligation! This has impact especially in delicate situations, like insolvency

of a group, where up- or cross-stream loans have been made between different legal firms; of course it is also an important topic for tax

reasons. That means, it’s also a transfer pricing matter.

Last but not least it has to be mentioned that in many countries there is no explicit duty to prepare a written loan agreement. For instance in

Switzerland art. 11 sect. 1 in connection with art. 312 OR. Even this happen in some laws it is very important to point out here that the

consequences of missing writings may lead to serious problems at the lender and also at the borrower!

Legal Questions

1.

Liability questions - wrong issued or booked loans my lead to serious problems!

2.

Tax questions - transfer pricing: regarding internal loans; dependent on the direction (see above) there may be too high or to low

interest rates applied and may be considered from the the tax departement as a hidden dividend.

3.

Documentation - is a written (legal binding) loan agreement issued and in case of prolongation, correct adjusted?

Contents of a Loan

Every on commercial basic principles based loan should consider the following points:

1.

Lender

2.

Borrower

3.

Date of Agreement

4.

Currency

5.

Amount

6.

Start- and Enddate

7.

Reference

8.

Nature of the loan (internal or external)

9.

Day count convention (Act/360, 30/360, Act/365, Act/Act)

10.

Interest definition (p.a., s.a.)

11.

Interst payment (fix, monthly, semi-annually etc.)

12.

Fix- or floating legs

13.

Account of the lender

14.

Account of the borrower

15.

A free text for remarks

16.

Interest fixing dates

17.

Authorized signatures

Snake-Pits in the interest calculation

Mainly corporates which have no specialized treasury software (e.g. our system STS) calculate the interest in Excel and make sometimes

errors in the interest calculation. In the following the main problem posings:

Day Count Convention

Depending on the currency and the duration of the loan there are different methods of calculating interest based on international best

practice standards.

Example: Short-Term Loan, EUR for 1/2 year, 31.12.15 - 30.06.16 (2016 is a lump leap year)

1.

Act/360

(1’000’000 x 1.0% x 182) / 360 x 100 = 5’055.56

2.

30/360

(1’000’000 x 1.0% x 180) / 360 x 100 = 5’000.00

3.

Act/365

(1’000’000 x 1.0% x 182) / 365 x 100 = 4’986.30

4.

Act/Act

(1’000’000 x 1.0% x 182) / 366 x 100 = 4’972.68

In this example for the short-term loan in EUR for 1/2 year the day count convention act/360 is correct. If others are applied, e.g. because of

a lack of professional knowledge, wrong interest is applied.

Time

We often saw in financial departments the problem that days are calculated wrong at all.

Example: A loan is agreed from Jan. 1st 2016 - Mar. 31st 2016 and is going to be prolongated until Jun. 30th 2016.

1.

01.01.16 - 31.03.16 and 01.04.16 - 30.06.16 = 90 days + 90 days = 180 days

-> that’s wrong in two ways:

a) Interest calculation starts just at the date when the funds are on the account of the borrower (valude date, not booking date). On

01.01.xx ni a year in most of the countries of the world this is no working day, hence there can’t be a credit on the account; earliest at

02.01.xx. But because 02.01.16 is a saturday (we assume, the loan is between a british- and a german company), the amount can be

credited earliest on 04.01.2016.

b) Between 31.03.16 and 01.04.2016 no interest was calculated.

2.

04.01.16 - 31.03.16 und 31.03.16 - 30.06.16 = 87 days + 91 days = 178 days.

Correct.

Interest Fixings

The most applied interest sources are the official fixings for instance LIBOR or EURIBOR. Those rates cover the period up to one year in

different time grids.

LIBOR: Overnight, 1 Week, 2 Weeks und then 1, 2, 3 ..12 Months

EURIBOR: 1 Week, 2 Weeks, 3 Weeks und then 1, 2, 3 .. 12 Months

Important to know is at a fixing that there is a difference between FIXING-DATE und VALUE-DATE. The Fixing-Date is always 2 working

days (of the currency, not the country) prior the date when funds are physically transferred.

Examples:

3.

01.01.16 -> Value Date Monday, 04.01.16 -> Zinsfixing = Wednesday, 30.12.2015

4.

15.03.16 -> Value Date Tuesday, 15.03.16 -> Zinsfixing = Friday, 11.03.16

Last but not least: always distinguish between booking and value-date!

Contact us, we would be glad to show you the possible opportunities!

often comprehensive questions arise which lead sometimes to serious problems because of a lack of technical knowledge and/or legal

understandings.

Fundamentials

Technical

This small mindmap shows that a loan has many facings. Dependent, what the goal of a loans is, many different details should be

considered carefully:

Technical Questions

1.

Interest source, e.g. from a newspaper or not approved google hits instead of a common market source - e.g. LIBOR, EURIBOR etc.

2.

Interest calculation, e.g. because of the currency and duration the correct day-count coventions need to be applied.

3.

Fundamential calculations, e.g. a loan which started at 30.06.xx and ends at 31.12.xx with a prolongation to 30.06.yy is calculated

30.12.xx - 31.12.xx and 01.01.yy - 30.06.yy. Here, one day is missing, the day from 31.12.xx- 01.01.yy!

Legal Aspects

The following explanations refer to the greatest possible extend on commercial law from 1. World

countries, e.g. Middle-Europe, North-America. But dependent on the specific country there may be

clear differences in the local law!

The substantial characteristics of a (money)loan is the obligation of the lender to deliver to the

borrower a certain amount for a specific time by transfer of ownership (delivery-obligation) and the

borrower has the obligation to repay the amount at the end (re-payment obligation). Additionally it

is an essential attribute of the lender to leave the amount during the live-time of the loan at the

borrower (relinquish-obligation).

However, the interest is for a loan not necessarely to be defined, as exiting it may sound in the first moment. Because interest is not equal

the loan, it is a separate item, i.e. the compensation of the lender for the usage of capital (= loan) during a certain period of time. So, in

common affairs interest is just payable if they had been agreed. Basically. But: in most of the laws there is an additional clause which says

that in commercial business interest is payable also without a special agreement.

Interest has additionally fundamential legal characteristics: If an agreement for interest is missing, one may conclude that it is in fact not a

loan in common sense, hence a repayment of the loan is not an obligation! This has impact especially in delicate situations, like insolvency

of a group, where up- or cross-stream loans have been made between different legal firms; of course it is also an important topic for tax

reasons. That means, it’s also a transfer pricing matter.

Last but not least it has to be mentioned that in many countries there is no explicit duty to prepare a written loan agreement. For instance in

Switzerland art. 11 sect. 1 in connection with art. 312 OR. Even this happen in some laws it is very important to point out here that the

consequences of missing writings may lead to serious problems at the lender and also at the borrower!

Legal Questions

1.

Liability questions - wrong issued or booked loans my lead to serious problems!

2.

Tax questions - transfer pricing: regarding internal loans; dependent on the direction (see above) there may be too high or to low

interest rates applied and may be considered from the the tax departement as a hidden dividend.

3.

Documentation - is a written (legal binding) loan agreement issued and in case of prolongation, correct adjusted?

Contents of a Loan

Every on commercial basic principles based loan should consider the following points:

1.

Lender

2.

Borrower

3.

Date of Agreement

4.

Currency

5.

Amount

6.

Start- and Enddate

7.

Reference

8.

Nature of the loan (internal or external)

9.

Day count convention (Act/360, 30/360, Act/365, Act/Act)

10.

Interest definition (p.a., s.a.)

11.

Interst payment (fix, monthly, semi-annually etc.)

12.

Fix- or floating legs

13.

Account of the lender

14.

Account of the borrower

15.

A free text for remarks

16.

Interest fixing dates

17.

Authorized signatures

Snake-Pits in the interest calculation

Mainly corporates which have no specialized treasury software (e.g. our system STS) calculate the interest in Excel and make sometimes

errors in the interest calculation. In the following the main problem posings:

Day Count Convention

Depending on the currency and the duration of the loan there are different methods of calculating interest based on international best

practice standards.

Example: Short-Term Loan, EUR for 1/2 year, 31.12.15 - 30.06.16 (2016 is a lump leap year)

1.

Act/360

(1’000’000 x 1.0% x 182) / 360 x 100 = 5’055.56

2.

30/360

(1’000’000 x 1.0% x 180) / 360 x 100 = 5’000.00

3.

Act/365

(1’000’000 x 1.0% x 182) / 365 x 100 = 4’986.30

4.

Act/Act

(1’000’000 x 1.0% x 182) / 366 x 100 = 4’972.68

In this example for the short-term loan in EUR for 1/2 year the day count convention act/360 is correct. If others are applied, e.g. because of

a lack of professional knowledge, wrong interest is applied.

Time

We often saw in financial departments the problem that days are calculated wrong at all.

Example: A loan is agreed from Jan. 1st 2016 - Mar. 31st 2016 and is going to be prolongated until Jun. 30th 2016.

1.

01.01.16 - 31.03.16 and 01.04.16 - 30.06.16 = 90 days + 90 days = 180 days

-> that’s wrong in two ways:

a) Interest calculation starts just at the date when the funds are on the account of the borrower (valude date, not booking date). On

01.01.xx ni a year in most of the countries of the world this is no working day, hence there can’t be a credit on the account; earliest at

02.01.xx. But because 02.01.16 is a saturday (we assume, the loan is between a british- and a german company), the amount can be

credited earliest on 04.01.2016.

b) Between 31.03.16 and 01.04.2016 no interest was calculated.

2.

04.01.16 - 31.03.16 und 31.03.16 - 30.06.16 = 87 days + 91 days = 178 days.

Correct.

Interest Fixings

The most applied interest sources are the official fixings for instance LIBOR or EURIBOR. Those rates cover the period up to one year in

different time grids.

LIBOR: Overnight, 1 Week, 2 Weeks und then 1, 2, 3 ..12 Months

EURIBOR: 1 Week, 2 Weeks, 3 Weeks und then 1, 2, 3 .. 12 Months

Important to know is at a fixing that there is a difference between FIXING-DATE und VALUE-DATE. The Fixing-Date is always 2 working

days (of the currency, not the country) prior the date when funds are physically transferred.

Examples:

3.

01.01.16 -> Value Date Monday, 04.01.16 -> Zinsfixing = Wednesday, 30.12.2015

4.

15.03.16 -> Value Date Tuesday, 15.03.16 -> Zinsfixing = Friday, 11.03.16

Last but not least: always distinguish between booking and value-date!

Contact us, we would be glad to show you the possible opportunities!

often comprehensive questions arise which lead sometimes to serious problems because of a lack of technical knowledge and/or legal

understandings.

Fundamentials

Technical

This small mindmap shows that a loan has many facings. Dependent, what the goal of a loans is, many different details should be

considered carefully:

Technical Questions

1.

Interest source, e.g. from a newspaper or not approved google hits instead of a common market source - e.g. LIBOR, EURIBOR etc.

2.

Interest calculation, e.g. because of the currency and duration the correct day-count coventions need to be applied.

3.

Fundamential calculations, e.g. a loan which started at 30.06.xx and ends at 31.12.xx with a prolongation to 30.06.yy is calculated

30.12.xx - 31.12.xx and 01.01.yy - 30.06.yy. Here, one day is missing, the day from 31.12.xx- 01.01.yy!

Legal Aspects

The following explanations refer to the greatest possible extend on commercial law from 1. World

countries, e.g. Middle-Europe, North-America. But dependent on the specific country there may be

clear differences in the local law!

The substantial characteristics of a (money)loan is the obligation of the lender to deliver to the

borrower a certain amount for a specific time by transfer of ownership (delivery-obligation) and the

borrower has the obligation to repay the amount at the end (re-payment obligation). Additionally it

is an essential attribute of the lender to leave the amount during the live-time of the loan at the

borrower (relinquish-obligation).

However, the interest is for a loan not necessarely to be defined, as exiting it may sound in the first moment. Because interest is not equal

the loan, it is a separate item, i.e. the compensation of the lender for the usage of capital (= loan) during a certain period of time. So, in

common affairs interest is just payable if they had been agreed. Basically. But: in most of the laws there is an additional clause which says

that in commercial business interest is payable also without a special agreement.

Interest has additionally fundamential legal characteristics: If an agreement for interest is missing, one may conclude that it is in fact not a

loan in common sense, hence a repayment of the loan is not an obligation! This has impact especially in delicate situations, like insolvency

of a group, where up- or cross-stream loans have been made between different legal firms; of course it is also an important topic for tax

reasons. That means, it’s also a transfer pricing matter.

Last but not least it has to be mentioned that in many countries there is no explicit duty to prepare a written loan agreement. For instance in

Switzerland art. 11 sect. 1 in connection with art. 312 OR. Even this happen in some laws it is very important to point out here that the

consequences of missing writings may lead to serious problems at the lender and also at the borrower!

Legal Questions

1.

Liability questions - wrong issued or booked loans my lead to serious problems!

2.

Tax questions - transfer pricing: regarding internal loans; dependent on the direction (see above) there may be too high or to low

interest rates applied and may be considered from the the tax departement as a hidden dividend.

3.

Documentation - is a written (legal binding) loan agreement issued and in case of prolongation, correct adjusted?

Contents of a Loan

Every on commercial basic principles based loan should consider the following points:

1.

Lender

2.

Borrower

3.

Date of Agreement

4.

Currency

5.

Amount

6.

Start- and Enddate

7.

Reference

8.

Nature of the loan (internal or external)

9.

Day count convention (Act/360, 30/360, Act/365, Act/Act)

10.

Interest definition (p.a., s.a.)

11.

Interst payment (fix, monthly, semi-annually etc.)

12.

Fix- or floating legs

13.

Account of the lender

14.

Account of the borrower

15.

A free text for remarks

16.

Interest fixing dates

17.

Authorized signatures

Snake-Pits in the interest calculation

Mainly corporates which have no specialized treasury software (e.g. our system STS) calculate the interest in Excel and make sometimes

errors in the interest calculation. In the following the main problem posings:

Day Count Convention

Depending on the currency and the duration of the loan there are different methods of calculating interest based on international best

practice standards.

Example: Short-Term Loan, EUR for 1/2 year, 31.12.15 - 30.06.16 (2016 is a lump leap year)

1.

Act/360

(1’000’000 x 1.0% x 182) / 360 x 100 = 5’055.56

2.

30/360

(1’000’000 x 1.0% x 180) / 360 x 100 = 5’000.00

3.

Act/365

(1’000’000 x 1.0% x 182) / 365 x 100 = 4’986.30

4.

Act/Act

(1’000’000 x 1.0% x 182) / 366 x 100 = 4’972.68

In this example for the short-term loan in EUR for 1/2 year the day count convention act/360 is correct. If others are applied, e.g. because of

a lack of professional knowledge, wrong interest is applied.

Time

We often saw in financial departments the problem that days are calculated wrong at all.

Example: A loan is agreed from Jan. 1st 2016 - Mar. 31st 2016 and is going to be prolongated until Jun. 30th 2016.

1.

01.01.16 - 31.03.16 and 01.04.16 - 30.06.16 = 90 days + 90 days = 180 days

-> that’s wrong in two ways:

a) Interest calculation starts just at the date when the funds are on the account of the borrower (valude date, not booking date). On

01.01.xx ni a year in most of the countries of the world this is no working day, hence there can’t be a credit on the account; earliest at

02.01.xx. But because 02.01.16 is a saturday (we assume, the loan is between a british- and a german company), the amount can be

credited earliest on 04.01.2016.

b) Between 31.03.16 and 01.04.2016 no interest was calculated.

2.

04.01.16 - 31.03.16 und 31.03.16 - 30.06.16 = 87 days + 91 days = 178 days.

Correct.

Interest Fixings

The most applied interest sources are the official fixings for instance LIBOR or EURIBOR. Those rates cover the period up to one year in

different time grids.

LIBOR: Overnight, 1 Week, 2 Weeks und then 1, 2, 3 ..12 Months

EURIBOR: 1 Week, 2 Weeks, 3 Weeks und then 1, 2, 3 .. 12 Months

Important to know is at a fixing that there is a difference between FIXING-DATE und VALUE-DATE. The Fixing-Date is always 2 working

days (of the currency, not the country) prior the date when funds are physically transferred.

Examples:

3.

01.01.16 -> Value Date Monday, 04.01.16 -> Zinsfixing = Wednesday, 30.12.2015

4.

15.03.16 -> Value Date Tuesday, 15.03.16 -> Zinsfixing = Friday, 11.03.16

Last but not least: always distinguish between booking and value-date!

Contact us, we would be glad to show you the possible opportunities!

Loans

Loans - that’s something everybody seems to know and understand.

Not necessarely! The practice often shows considerable

comprehension questions.

Loans are considered generally often as fiddling, totally intelligible

and more over, as a simple financial agreement. But in practice

quite often comprehensive questions arise which lead sometimes to

serious problems because of a lack of technical knowledge and/or

legal understandings.

Fundamentials

Technical

(Please have a look to this site also on a Desktop-Screen and review

the Mind Map to undermentioned points, because this site is

optimized for Smartphones / Tablets)

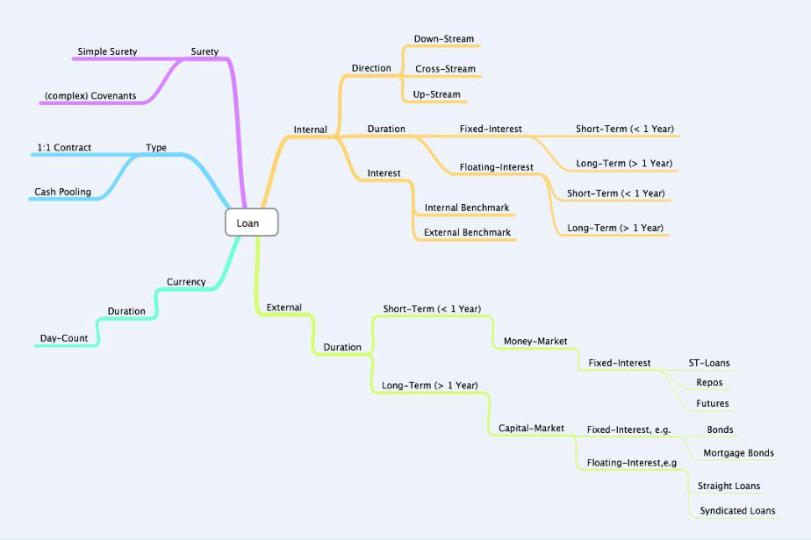

Loans are segregated primary for

1.

Internal / External

2.

Type

3.

Currency

4.

Surety

•

Secondly by direction -> Down-/Cross-/Upstream;

•

Duration -> Short Term < 1 Year und Long Term > 1 Year;

•

Fix or floating interest;

•

Interest benchmark -> internal or external;

•

Interest environment -> Money Market or Capital Market;

•

Instruments -> from fix loans through Repos, Bonds up to

syndicated Loans;

•

Day Count

•

Kind of Loan -> 1:1 or Cash Pooling

•

Kind of Surety -> simple or complex Coventants

This small mindmap shows that a loan has many facings.

Dependent, what the goal of a loans is, many different details should

be considered carefully:

Technical Questions

1.

Interest source, e.g. from a newspaper or not approved google

hits instead of a common market source - e.g. LIBOR,

EURIBOR etc.

2.

Interest calculation, e.g.

because of the currency

and duration the correct

day-count coventions

need to be applied.

3.

Fundamential

calculations, e.g. a loan

which started at

30.06.xx and ends at

31.12.xx with a prolongation to 30.06.yy is calculated 30.12.xx

- 31.12.xx and 01.01.yy - 30.06.yy. Here, one day is missing,

the day from 31.12.xx- 01.01.yy!

Legal Aspects

The following explanations refer to the greatest possible extend on

commercial law from 1. World countries, e.g. Middle-Europe, North-

America. But dependent on the specific country there may be clear

differences in the local law!

The substantial characteristics of a (money)loan is the obligation of

the lender to deliver to the borrower a certain amount for a specific

time by transfer of ownership (delivery-obligation) and the borrower

has the obligation to repay the amount at the end (re-payment

obligation). Additionally it is an essential attribute of the lender to

leave the amount during the live-time of the loan at the borrower

(relinquish-obligation).

However, the interest is for a loan not necessarely to be defined, as

exiting it may sound in the first moment. Because interest is not

equal the loan, it is a separate item, i.e. the compensation of the

lender for the usage of capital (= loan) during a certain period of

time. So, in common affairs interest is just payable if they had been

agreed. Basically. But: in most of the laws there is an additional

clause which says that in commercial business interest is payable

also without a special agreement.

Interest has additionally fundamential legal characteristics: If an

agreement for interest is missing, one may conclude that it is in fact

not a loan in common sense, hence a repayment of the loan is not

an obligation! This has impact especially in delicate situations, like

insolvency of a group, where up- or cross-stream loans have been

made between different legal firms; of course it is also an important

topic for tax reasons. That means, it’s also a transfer pricing matter.

Last but not least it has to be mentioned that in many countries there

is no explicit duty to prepare a written loan agreement. For instance

in Switzerland art. 11 sect. 1 in connection with art. 312 OR. Even

this happen in some laws it is very important to point out here that

the consequences of missing writings may lead to serious problems

at the lender and also at the borrower!

Legal Questions

1.

Liability questions - wrong issued or booked loans my lead to

serious problems!

2.

Tax questions - transfer pricing: regarding internal loans;

dependent on the direction (see above) there may be too high

or to low interest rates applied and may be considered from

the the tax departement as a hidden dividend.

3.

Documentation - is a written (legal binding) loan agreement

issued and in case of prolongation, correct adjusted?

Contents of a Loan

Every on commercial basic principles based loan should consider the

following points:

1.

Lender

2.

Borrower

3.

Date of Agreement

4.

Currency

5.

Amount

6.

Start- and Enddate

7.

Reference

8.

Nature of the loan (internal or external)

9.

Day count convention (Act/360, 30/360, Act/365, Act/Act)

10.

Interest definition (p.a., s.a.)

11.

Interst payment (fix, monthly, semi-annually etc.)

12.

Fix- or floating legs

13.

Account of the lender

14.

Account of the borrower

15.

A free text for remarks

16.

Interest fixing dates

17.

Authorized signatures

Snake-Pits in the interest calculation

Mainly corporates which have no specialized treasury software (e.g.

our system STS) calculate the interest in Excel and make sometimes

errors in the interest calculation. In the following the main problem

posings:

Day Count Convention

Depending on the currency and the duration of the loan there are

different methods of calculating interest based on international best

practice standards.

Example: Short-Term Loan, EUR for 1/2 year, 31.12.15 - 30.06.16

(2016 is a lump leap year)

1.

Act/360

(1’000’000 x 1.0% x 182) / 360 x 100 = 5’055.56

2.

30/360

(1’000’000 x 1.0% x 180) / 360 x 100 = 5’000.00

3.

Act/365

(1’000’000 x 1.0% x 182) / 365 x 100 = 4’986.30

4.

Act/Act

(1’000’000 x 1.0% x 182) / 366 x 100 = 4’972.68

In this example for the short-term loan in EUR for 1/2 year the day

count convention act/360 is correct. If others are applied, e.g.

because of a lack of professional knowledge, wrong interest is

applied.

Time

We often saw in financial departments the problem that days are

calculated wrong at all.

Example: A loan is agreed from Jan. 1st 2016 - Mar. 31st 2016 and

is going to be prolongated until Jun. 30th 2016.

1.

01.01.16 - 31.03.16 and 01.04.16 - 30.06.16 = 90 days + 90

days = 180 days

-> that’s wrong in two ways:

a) Interest calculation starts just at the date when the funds are

on the account of the borrower (valude date, not booking

date). On 01.01.xx ni a year in most of the countries of the

world this is no working day, hence there can’t be a credit on

the account; earliest at 02.01.xx. But because 02.01.16 is a

saturday (we assume, the loan is between a british- and a

german company), the amount can be credited earliest on

04.01.2016.

b) Between 31.03.16 and 01.04.2016 no interest was

calculated.

2.

04.01.16 - 31.03.16 und 31.03.16 - 30.06.16 = 87 days + 91

days = 178 days.

Correct.

Interest Fixings

The most applied interest sources are the official fixings for instance

LIBOR or EURIBOR. Those rates cover the period up to one year in

different time grids.

LIBOR: Overnight, 1 Week, 2 Weeks und then 1, 2, 3 ..12 Months

EURIBOR: 1 Week, 2 Weeks, 3 Weeks und then 1, 2, 3 .. 12 Months

Important to know is at a fixing that there is a difference between

FIXING-DATE und VALUE-DATE. The Fixing-Date is always 2

working days (of the currency, not the country) prior the date when

funds are physically transferred.

Examples:

3.

01.01.16 -> Value Date Monday, 04.01.16 -> Zinsfixing =

Wednesday, 30.12.2015

4.

15.03.16 -> Value Date Tuesday, 15.03.16 -> Zinsfixing =

Friday, 11.03.16

Last but not least: always distinguish between booking and value-

date!

Contact us, we would be glad to show you the possible

opportunities!

and more over, as a simple financial agreement. But in practice

quite often comprehensive questions arise which lead sometimes to

serious problems because of a lack of technical knowledge and/or

legal understandings.

Fundamentials

Technical

(Please have a look to this site also on a Desktop-Screen and review

the Mind Map to undermentioned points, because this site is

optimized for Smartphones / Tablets)

Loans are segregated primary for

1.

Internal / External

2.

Type

3.

Currency

4.

Surety

•

Secondly by direction -> Down-/Cross-/Upstream;

•

Duration -> Short Term < 1 Year und Long Term > 1 Year;

•

Fix or floating interest;

•

Interest benchmark -> internal or external;

•

Interest environment -> Money Market or Capital Market;

•

Instruments -> from fix loans through Repos, Bonds up to

syndicated Loans;

•

Day Count

•

Kind of Loan -> 1:1 or Cash Pooling

•

Kind of Surety -> simple or complex Coventants

This small mindmap shows that a loan has many facings.

Dependent, what the goal of a loans is, many different details should

be considered carefully:

Technical Questions

1.

Interest source, e.g. from a newspaper or not approved google

hits instead of a common market source - e.g. LIBOR,

EURIBOR etc.

2.

Interest calculation, e.g.

because of the currency

and duration the correct

day-count coventions

need to be applied.

3.

Fundamential

calculations, e.g. a loan

which started at

30.06.xx and ends at

31.12.xx with a prolongation to 30.06.yy is calculated 30.12.xx

- 31.12.xx and 01.01.yy - 30.06.yy. Here, one day is missing,

the day from 31.12.xx- 01.01.yy!

Legal Aspects

The following explanations refer to the greatest possible extend on

commercial law from 1. World countries, e.g. Middle-Europe, North-

America. But dependent on the specific country there may be clear

differences in the local law!

The substantial characteristics of a (money)loan is the obligation of

the lender to deliver to the borrower a certain amount for a specific

time by transfer of ownership (delivery-obligation) and the borrower

has the obligation to repay the amount at the end (re-payment

obligation). Additionally it is an essential attribute of the lender to

leave the amount during the live-time of the loan at the borrower

(relinquish-obligation).

However, the interest is for a loan not necessarely to be defined, as

exiting it may sound in the first moment. Because interest is not

equal the loan, it is a separate item, i.e. the compensation of the

lender for the usage of capital (= loan) during a certain period of

time. So, in common affairs interest is just payable if they had been

agreed. Basically. But: in most of the laws there is an additional

clause which says that in commercial business interest is payable

also without a special agreement.

Interest has additionally fundamential legal characteristics: If an

agreement for interest is missing, one may conclude that it is in fact

not a loan in common sense, hence a repayment of the loan is not

an obligation! This has impact especially in delicate situations, like

insolvency of a group, where up- or cross-stream loans have been

made between different legal firms; of course it is also an important

topic for tax reasons. That means, it’s also a transfer pricing matter.

Last but not least it has to be mentioned that in many countries there

is no explicit duty to prepare a written loan agreement. For instance

in Switzerland art. 11 sect. 1 in connection with art. 312 OR. Even

this happen in some laws it is very important to point out here that

the consequences of missing writings may lead to serious problems

at the lender and also at the borrower!

Legal Questions

1.

Liability questions - wrong issued or booked loans my lead to

serious problems!

2.

Tax questions - transfer pricing: regarding internal loans;

dependent on the direction (see above) there may be too high

or to low interest rates applied and may be considered from

the the tax departement as a hidden dividend.

3.

Documentation - is a written (legal binding) loan agreement

issued and in case of prolongation, correct adjusted?

Contents of a Loan

Every on commercial basic principles based loan should consider the

following points:

1.

Lender

2.

Borrower

3.

Date of Agreement

4.

Currency

5.

Amount

6.

Start- and Enddate

7.

Reference

8.

Nature of the loan (internal or external)

9.

Day count convention (Act/360, 30/360, Act/365, Act/Act)

10.

Interest definition (p.a., s.a.)

11.

Interst payment (fix, monthly, semi-annually etc.)

12.

Fix- or floating legs

13.

Account of the lender

14.

Account of the borrower

15.

A free text for remarks

16.

Interest fixing dates

17.

Authorized signatures

Snake-Pits in the interest calculation

Mainly corporates which have no specialized treasury software (e.g.

our system STS) calculate the interest in Excel and make sometimes

errors in the interest calculation. In the following the main problem

posings:

Day Count Convention

Depending on the currency and the duration of the loan there are

different methods of calculating interest based on international best

practice standards.

Example: Short-Term Loan, EUR for 1/2 year, 31.12.15 - 30.06.16

(2016 is a lump leap year)

1.

Act/360

(1’000’000 x 1.0% x 182) / 360 x 100 = 5’055.56

2.

30/360

(1’000’000 x 1.0% x 180) / 360 x 100 = 5’000.00

3.

Act/365

(1’000’000 x 1.0% x 182) / 365 x 100 = 4’986.30

4.

Act/Act

(1’000’000 x 1.0% x 182) / 366 x 100 = 4’972.68

In this example for the short-term loan in EUR for 1/2 year the day

count convention act/360 is correct. If others are applied, e.g.

because of a lack of professional knowledge, wrong interest is

applied.

Time

We often saw in financial departments the problem that days are

calculated wrong at all.

Example: A loan is agreed from Jan. 1st 2016 - Mar. 31st 2016 and

is going to be prolongated until Jun. 30th 2016.

1.

01.01.16 - 31.03.16 and 01.04.16 - 30.06.16 = 90 days + 90

days = 180 days

-> that’s wrong in two ways:

a) Interest calculation starts just at the date when the funds are

on the account of the borrower (valude date, not booking

date). On 01.01.xx ni a year in most of the countries of the

world this is no working day, hence there can’t be a credit on

the account; earliest at 02.01.xx. But because 02.01.16 is a

saturday (we assume, the loan is between a british- and a

german company), the amount can be credited earliest on

04.01.2016.

b) Between 31.03.16 and 01.04.2016 no interest was

calculated.

2.

04.01.16 - 31.03.16 und 31.03.16 - 30.06.16 = 87 days + 91

days = 178 days.

Correct.

Interest Fixings

The most applied interest sources are the official fixings for instance

LIBOR or EURIBOR. Those rates cover the period up to one year in

different time grids.

LIBOR: Overnight, 1 Week, 2 Weeks und then 1, 2, 3 ..12 Months

EURIBOR: 1 Week, 2 Weeks, 3 Weeks und then 1, 2, 3 .. 12 Months

Important to know is at a fixing that there is a difference between

FIXING-DATE und VALUE-DATE. The Fixing-Date is always 2

working days (of the currency, not the country) prior the date when

funds are physically transferred.

Examples:

3.

01.01.16 -> Value Date Monday, 04.01.16 -> Zinsfixing =

Wednesday, 30.12.2015

4.

15.03.16 -> Value Date Tuesday, 15.03.16 -> Zinsfixing =

Friday, 11.03.16

Last but not least: always distinguish between booking and value-

date!

Contact us, we would be glad to show you the possible

opportunities!