Cash Pooling

Increase the liquidity, improve interest result and reduce external debts,

this is common do be achieved with Cash Pooling. As Zero-Balancing, Target-Balancing

or Notional Cash Pooling.

The primary target of each cash pooling is the optimization and use of surplus funds of all companies in a group in order to reduce external debt and increase the available liquidity. Furthermore, especially interest benefits in multiple ways can be achieved for the pool participants

on the payable and on the receivable side.

Type 1: Zero- or Target Balancing Cash Pool (physical)

The zero-balancing, also called cash-concentration or sweeping, is in his form the easiest way to introduce cash pooling. Depending on a

surplus or lack of cash, all cash balances in the Pool (Pool-Participants) will be transferred on daily basis automatic to or from the top-

mother account (Pool-Leader). A major positive effect is a shorter balance and therefore the key-figure of the debt-ratio improves. But there

are also some disadvantages, e.g. liability-questions in case of a short-fall of the pool-leader (see Erb-Group and Swissair in

Switzerland or Bremer Vulkan in Germany). Also there is a higher administrative work since all intercompany cash flows on a daily level

have to be booked at the pool-leader (can be automatized). The key-element of a zero- or target balancing is that all cash flows are

physicly.

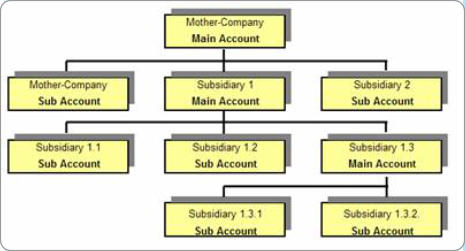

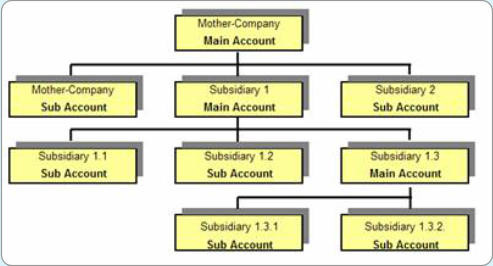

Setup of a Zero-Balancing-Pool

It is also important to respect tax considerations, i.e. transfer pricing. Because as already mentioned, the “classic” cash pooling is simply an

automatic loan transaction on daily basis. Some countries, also in Europe, have laws that either interest payment and/or loans in the

one or other direction are prohibited or even do not allow physical cash flows. This is typically a process of multinational groups and has

negative impact on cross border transactions.

Process / Functionality of a Zero- or Target Cash Pool

Pooling Accounts of the Participants can be regulated in two ways, both fully automatic:

a) Zero-Balancing: all participating accounts, except the header-account, are set to 0 (zero) at the end of a day. Surplus balances are

debited, minus balances are credited to/from the header account.

b) Target-Balancing: basically the same procedure as with zero-balancing, just with a number of extended parameter regarding the day-

end balance. For example every day a pre-defined balance remain on the account, which may be for instance used for lease-guarantee

etc.

Because of technical restrictions all transfers can be

booked at the next following day, but will be execured

always with the correct value date.

Here an example, how the communications for the

transfer of balances may happen through the SWIFT-

Network. Dependent from the executing Banks some

differences can be the case. It is also often the case

that the cash pool can be not managed by only one

Bank, because the House-Bank has not in every

country a branch. This is commonly the case in

Cross-Border Pools, see below. That means a third

Bank must be included in the pool-network.

This example is certainly strong simplified und

contains for instance no internal connections which

are mandatory in the accounting of the Pool-Leader

an all Subsidiaries.

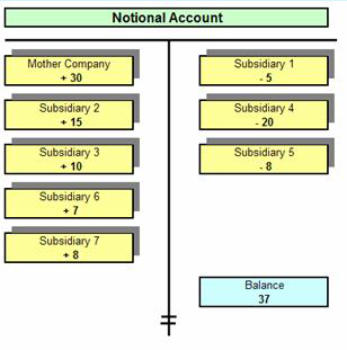

Type 2: Notional Cash Pool (no physical transfer of funds)

The meaning of „notional“ name it: this pooling form is not real. But is is a 100% interest optimization. There are no physical transfers

between the accounts. The single balance accounts will be added together and netted against each other. Therefore each pool participant

has his own bankaccount with the full physical balance, but the full interest spread remain within the group.

Therefore this kind of pooling meets perfect the needs of companies which does not like to enter into any credit risk! In a few words:

interest optimization without having the character of loans and related risks.

An extended version of this pooling is a combination of different currencies in one and the same cash-pool. Some Banks offer this service,

ask us for assistance. Technically, the Bank is just entereing into a number of overnight-swaps.

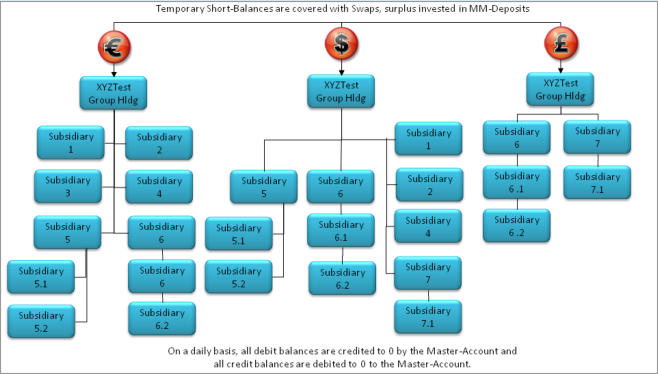

Complex Topic: Cross Border Cash Pooling

A well tuned cash pool structure may not only transfer cash over the border, it can do it even in different currencies! So it is possible to

establish a cash pool for EUR, one for for CHF and one for USD. All cash flows will be transferred to / from the ultimate mother group

account on daily basis and will be managed by the Treasurer as portfolio to cover gaps on daily or weekly with swaps, without entering

into any foreign exchange risk!

Cross-Border Pooling is certainly the biggest advantage for a cash management who wants to generate a maximum benefit out of the cash

pool. But also the risk increase and therewith related, the ultimate accuracy for setting up or manage cross-border pools. Risk has per

definition the attribute as getting larger as more parameters need to be considered. The adavantages and disadvantages are different from

company to company, depending on the structure and planned pooling type. For instance, the right bank on your side is very important. To

find out who this bank could be is described here. In the the following just a view arguments in a SWOT analysis which should be

considered very carefully:

Controlling

Be aware - cash pooling can be also a threat if rights and liabilites are not clearly defined. For this we recommend a comprehensive

Treasuy Policy - see here.

Software Support

A proper management of a cash pooling may become quite complex if there is no sufficient support by an adequated software. See here

how Cash Pooling can be managed easy and safe with the Cash Pool Module in our Treasury Software STS.

Country specific Items

Depending on the country where the bank-account for the cash pool is established, it is fully, partially or not allowed to operate such a pool.

Based on our experience with cash pool projects world wide we composed a manuscript which gives an overview about the different

country-specifications. Read more in detail here.

Reasons for Cash Pooling

Optimal allocation of internal liquid funds and max. reduction of external debts,

•

Reduction of financing costs on group level,

•

Improvement of investment return due to economies of scale,

•

Simplification of liquiditymanagagement on local level,

•

Reduction of external banking costs due to centralization,

•

Optimization of cash flow forecast because of coordination of financing cycles,

•

Break-Even of a cash pool starts at around 300’000.- required capital.

Contact us, we would be glad to show you the possible opportunities!

debt and increase the available liquidity. Furthermore, especially interest benefits in multiple ways can be achieved for the pool participants

on the payable and on the receivable side.

Type 1: Zero- or Target Balancing Cash Pool (physical)

The zero-balancing, also called cash-concentration or sweeping, is in his form the easiest way to introduce cash pooling. Depending on a

surplus or lack of cash, all cash balances in the Pool (Pool-Participants) will be transferred on daily basis automatic to or from the top-

mother account (Pool-Leader). A major positive effect is a shorter balance and therefore the key-figure of the debt-ratio improves. But there

are also some disadvantages, e.g. liability-questions in case of a short-fall of the pool-leader (see Erb-Group and Swissair in

Switzerland or Bremer Vulkan in Germany). Also there is a higher administrative work since all intercompany cash flows on a daily level

have to be booked at the pool-leader (can be automatized). The key-element of a zero- or target balancing is that all cash flows are

physicly.

Setup of a Zero-Balancing-Pool

It is also important to respect tax considerations, i.e. transfer pricing. Because as already mentioned, the “classic” cash pooling is simply an

automatic loan transaction on daily basis. Some countries, also in Europe, have laws that either interest payment and/or loans in the

one or other direction are prohibited or even do not allow physical cash flows. This is typically a process of multinational groups and has

negative impact on cross border transactions.

Process / Functionality of a Zero- or Target Cash Pool

Pooling Accounts of the Participants can be regulated in two ways, both fully automatic:

a) Zero-Balancing: all participating accounts, except the header-account, are set to 0 (zero) at the end of a day. Surplus balances are

debited, minus balances are credited to/from the header account.

b) Target-Balancing: basically the same procedure as with zero-balancing, just with a number of extended parameter regarding the day-

end balance. For example every day a pre-defined balance remain on the account, which may be for instance used for lease-guarantee

etc.

Because of technical restrictions all transfers can be

booked at the next following day, but will be execured

always with the correct value date.

Here an example, how the communications for the

transfer of balances may happen through the SWIFT-

Network. Dependent from the executing Banks some

differences can be the case. It is also often the case

that the cash pool can be not managed by only one

Bank, because the House-Bank has not in every

country a branch. This is commonly the case in

Cross-Border Pools, see below. That means a third

Bank must be included in the pool-network.

This example is certainly strong simplified und

contains for instance no internal connections which

are mandatory in the accounting of the Pool-Leader

an all Subsidiaries.

Type 2: Notional Cash Pool (no physical transfer of funds)

The meaning of „notional“ name it: this pooling form is not real. But is is a 100% interest optimization. There are no physical transfers

between the accounts. The single balance accounts will be added together and netted against each other. Therefore each pool participant

has his own bankaccount with the full physical balance, but the full interest spread remain within the group.

Therefore this kind of pooling meets perfect the needs of companies which does not like to enter into any credit risk! In a few words:

interest optimization without having the character of loans and related risks.

An extended version of this pooling is a combination of different currencies in one and the same cash-pool. Some Banks offer this service,

ask us for assistance. Technically, the Bank is just entereing into a number of overnight-swaps.

Complex Topic: Cross Border Cash Pooling

A well tuned cash pool structure may not only transfer cash over the border, it can do it even in different currencies! So it is possible to

establish a cash pool for EUR, one for for CHF and one for USD. All cash flows will be transferred to / from the ultimate mother group

account on daily basis and will be managed by the Treasurer as portfolio to cover gaps on daily or weekly with swaps, without entering

into any foreign exchange risk!

Cross-Border Pooling is certainly the biggest advantage for a cash management who wants to generate a maximum benefit out of the cash

pool. But also the risk increase and therewith related, the ultimate accuracy for setting up or manage cross-border pools. Risk has per

definition the attribute as getting larger as more parameters need to be considered. The adavantages and disadvantages are different from

company to company, depending on the structure and planned pooling type. For instance, the right bank on your side is very important. To

find out who this bank could be is described here. In the the following just a view arguments in a SWOT analysis which should be

considered very carefully:

Controlling

Be aware - cash pooling can be also a threat if rights and liabilites are not clearly defined. For this we recommend a comprehensive

Treasuy Policy - see here.

Software Support

A proper management of a cash pooling may become quite complex if there is no sufficient support by an adequated software. See here

how Cash Pooling can be managed easy and safe with the Cash Pool Module in our Treasury Software STS.

Country specific Items

Depending on the country where the bank-account for the cash pool is established, it is fully, partially or not allowed to operate such a pool.

Based on our experience with cash pool projects world wide we composed a manuscript which gives an overview about the different

country-specifications. Read more in detail here.

Reasons for Cash Pooling

Optimal allocation of internal liquid funds and max. reduction of external debts,

•

Reduction of financing costs on group level,

•

Improvement of investment return due to economies of scale,

•

Simplification of liquiditymanagagement on local level,

•

Reduction of external banking costs due to centralization,

•

Optimization of cash flow forecast because of coordination of financing cycles,

•

Break-Even of a cash pool starts at around 300’000.- required capital.

Contact us, we would be glad to show you the possible opportunities!

debt and increase the available liquidity. Furthermore, especially interest benefits in multiple ways can be achieved for the pool participants

on the payable and on the receivable side.

Type 1: Zero- or Target Balancing Cash Pool (physical)

The zero-balancing, also called cash-concentration or sweeping, is in his form the easiest way to introduce cash pooling. Depending on a

surplus or lack of cash, all cash balances in the Pool (Pool-Participants) will be transferred on daily basis automatic to or from the top-

mother account (Pool-Leader). A major positive effect is a shorter balance and therefore the key-figure of the debt-ratio improves. But there

are also some disadvantages, e.g. liability-questions in case of a short-fall of the pool-leader (see Erb-Group and Swissair in

Switzerland or Bremer Vulkan in Germany). Also there is a higher administrative work since all intercompany cash flows on a daily level

have to be booked at the pool-leader (can be automatized). The key-element of a zero- or target balancing is that all cash flows are

physicly.

Setup of a Zero-Balancing-Pool

It is also important to respect tax considerations, i.e. transfer pricing. Because as already mentioned, the “classic” cash pooling is simply an

automatic loan transaction on daily basis. Some countries, also in Europe, have laws that either interest payment and/or loans in the

one or other direction are prohibited or even do not allow physical cash flows. This is typically a process of multinational groups and has

negative impact on cross border transactions.

Process / Functionality of a Zero- or Target Cash Pool

Pooling Accounts of the Participants can be regulated in two ways, both fully automatic:

a) Zero-Balancing: all participating accounts, except the header-account, are set to 0 (zero) at the end of a day. Surplus balances are

debited, minus balances are credited to/from the header account.

b) Target-Balancing: basically the same procedure as with zero-balancing, just with a number of extended parameter regarding the day-

end balance. For example every day a pre-defined balance remain on the account, which may be for instance used for lease-guarantee

etc.

Because of technical restrictions all transfers can be

booked at the next following day, but will be execured

always with the correct value date.

Here an example, how the communications for the

transfer of balances may happen through the SWIFT-

Network. Dependent from the executing Banks some

differences can be the case. It is also often the case

that the cash pool can be not managed by only one

Bank, because the House-Bank has not in every

country a branch. This is commonly the case in

Cross-Border Pools, see below. That means a third

Bank must be included in the pool-network.

This example is certainly strong simplified und

contains for instance no internal connections which

are mandatory in the accounting of the Pool-Leader

an all Subsidiaries.

Type 2: Notional Cash Pool (no physical transfer of funds)

The meaning of „notional“ name it: this pooling form is not real. But is is a 100% interest optimization. There are no physical transfers

between the accounts. The single balance accounts will be added together and netted against each other. Therefore each pool participant

has his own bankaccount with the full physical balance, but the full interest spread remain within the group.

Therefore this kind of pooling meets perfect the needs of companies which does not like to enter into any credit risk! In a few words:

interest optimization without having the character of loans and related risks.

An extended version of this pooling is a combination of different currencies in one and the same cash-pool. Some Banks offer this service,

ask us for assistance. Technically, the Bank is just entereing into a number of overnight-swaps.

Complex Topic: Cross Border Cash Pooling

A well tuned cash pool structure may not only transfer cash over the border, it can do it even in different currencies! So it is possible to

establish a cash pool for EUR, one for for CHF and one for USD. All cash flows will be transferred to / from the ultimate mother group

account on daily basis and will be managed by the Treasurer as portfolio to cover gaps on daily or weekly with swaps, without entering

into any foreign exchange risk!

Cross-Border Pooling is certainly the biggest advantage for a cash management who wants to generate a maximum benefit out of the cash

pool. But also the risk increase and therewith related, the ultimate accuracy for setting up or manage cross-border pools. Risk has per

definition the attribute as getting larger as more parameters need to be considered. The adavantages and disadvantages are different from

company to company, depending on the structure and planned pooling type. For instance, the right bank on your side is very important. To

find out who this bank could be is described here. In the the following just a view arguments in a SWOT analysis which should be

considered very carefully:

Controlling

Be aware - cash pooling can be also a threat if rights and liabilites are not clearly defined. For this we recommend a comprehensive

Treasuy Policy - see here.

Software Support

A proper management of a cash pooling may become quite complex if there is no sufficient support by an adequated software. See here

how Cash Pooling can be managed easy and safe with the Cash Pool Module in our Treasury Software STS.

Country specific Items

Depending on the country where the bank-account for the cash pool is established, it is fully, partially or not allowed to operate such a pool.

Based on our experience with cash pool projects world wide we composed a manuscript which gives an overview about the different

country-specifications. Read more in detail here.

Reasons for Cash Pooling

Optimal allocation of internal liquid funds and max. reduction of external debts,

•

Reduction of financing costs on group level,

•

Improvement of investment return due to economies of scale,

•

Simplification of liquiditymanagagement on local level,

•

Reduction of external banking costs due to centralization,

•

Optimization of cash flow forecast because of coordination of financing cycles,

•

Break-Even of a cash pool starts at around 300’000.- required capital.

Contact us, we would be glad to show you the possible opportunities!

Cash Pooling

Increase the liquidity, improve interest result and reduce

external debts, this is common do be achieved with Cash

Pooling. As Zero-Balancing, Target-Balancing

or Notional Cash Pooling.

The primary target of each cash pooling is the optimization and use of

surplus funds of all companies in a group in order to reduce external

debt and increase the available liquidity. Furthermore, especially

interest benefits in multiple ways can be achieved for the pool

participants on the payable and on the receivable side.

Type 1: Zero- or Target Balancing Cash Pool

(physical)

The zero-balancing, also called cash-concentration or sweeping, is

in his form the easiest way to introduce cash pooling. Depending on a

surplus or lack of cash, all cash balances in the Pool (Pool-

Participants) will be transferred on daily basis automatic to or from

the top-mother account (Pool-Leader). A major positive effect is a

shorter balance and therefore the key-figure of the debt-ratio

improves. But there are also some disadvantages, e.g. liability-

questions in case of a short-fall of the pool-leader (see Erb-Group

and Swissair in Switzerland or Bremer Vulkan in Germany). Also

there is a higher administrative work since all intercompany cash

flows on a daily level have to be booked at the pool-leader (can be

automatized). The key-element of a zero- or target balancing is that

all cash flows are physicly.

Setup of a Zero-Balancing-Pool

It is also important to respect tax considerations, i.e. transfer pricing.

Because as already mentioned, the “classic” cash pooling is simply

an automatic loan transaction on daily basis. Some countries, also

in Europe, have laws that either interest payment and/or loans in the

one or other direction are prohibited or even do not allow physical

cash flows. This is typically a process of multinational groups and has

negative impact on cross border transactions.

Process / Functionality of a Zero- or Target Cash Pool

Pooling Accounts of the Participants can be regulated in two ways,

both fully automatic:

a) Zero-Balancing: all participating accounts, except the header-

account, are set to 0 (zero) at the end of a day. Surplus balances are

debited, minus balances are credited to/from the header account.

b) Target-Balancing: basically the same procedure as with zero-

balancing, just with a number of extended parameter regarding the

day-end balance. For example every day a pre-defined balance

remain on the account, which may be for instance used for lease-

guarantee etc.

Because of technical restrictions all transfers can be booked at the

next following day, but will be execured always with the correct value

date.

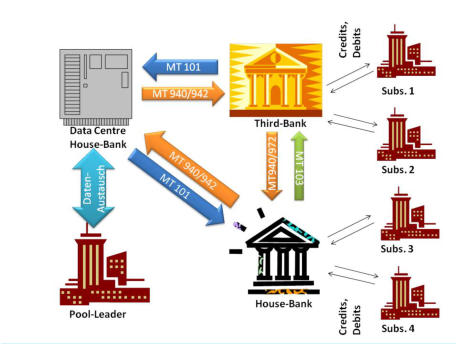

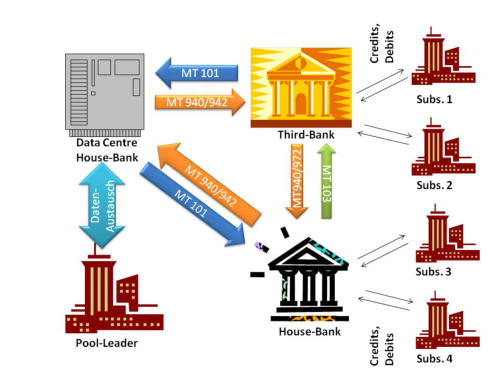

Here an example, how the communications for the transfer of

balances may happen through the SWIFT-Network. Dependent from

the executing Banks some differences can be the case. It is also

often the case that the cash pool can be not managed by only one

Bank, because the House-Bank has not in every country a branch.

This is commonly the case in Cross-Border Pools, see below. That

means a third Bank must be included in the pool-network.

This example is certainly strong simplified und contains for instance

no internal connections which are mandatory in the accounting of the

Pool-Leader an all Subsidiaries.

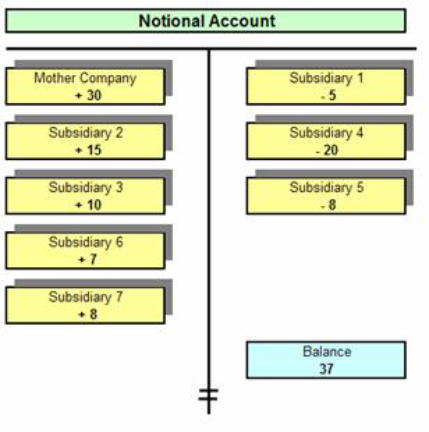

Type 2: Notional Cash Pool

(no physical transfer of funds)

The meaning of „notional“ name it: this pooling form is not real. But is

is a 100% interest optimization. There are no physical transfers

between the accounts. The single balance accounts will be added

together and netted against each other. Therefore each pool

participant has his own bankaccount with the full physical balance,

but the full interest spread remain within the group.

Therefore this kind of pooling meets perfect the needs of companies

which does not like to enter into any credit risk! In a few words:

interest optimization without having the character of loans and related

risks.

An extended version of this pooling is a combination of different

currencies in one and the same cash-pool. Some Banks offer this

service, ask us for assistance. Technically, the Bank is just entereing

into a number of overnight-swaps.

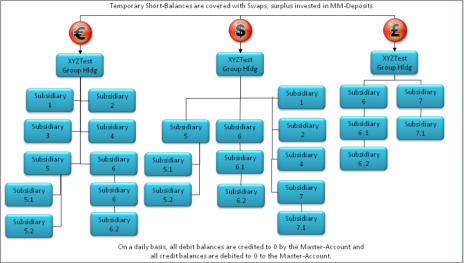

Complex Topic: Cross Border Cash Pooling

A well tuned cash pool structure may not only transfer cash over the

border, it can do it even in different currencies! So it is possible to

establish a cash pool for EUR, one for for CHF and one for USD. All

cash flows will be transferred to / from the ultimate mother group

account on daily basis and will be managed by the Treasurer as

portfolio to cover gaps on daily or weekly with swaps, without

entering into any foreign exchange risk!

Cross-Border Pooling is certainly the biggest advantage for a cash

management who wants to generate a maximum benefit out of the

cash pool. But also the risk increase and therewith related, the

ultimate accuracy for setting up or manage cross-border pools. Risk

has per definition the attribute as getting larger as more parameters

need to be considered. The adavantages and disadvantages are

different from company to company, depending on the structure and

planned pooling type. For instance, the right bank on your side is very

important. To find out who this bank could be is described here. In the

the following just a view arguments in a SWOT analysis which should

be considered very carefully:

Controlling

Be aware - cash pooling can be also a threat if rights and liabilites are

not clearly defined. For this we recommend a comprehensive Treasuy

Policy - see here.

Software Support

A proper management of a cash pooling may become quite complex

if there is no sufficient support by an adequated software. See here

how Cash Pooling can be managed easy and safe with the Cash Pool

Module in our Treasury Software STS.

Country specific Items

Depending on the country where the bank-account for the cash pool

is established, it is fully, partially or not allowed to operate such a

pool. Based on our experience with cash pool projects world wide we

composed a manuscript which gives an overview about the different

country-specifications. Read more in detail here.

Reasons for Cash Pooling

Optimal allocation of internal liquid funds and max. reduction of

external debts,

•

Reduction of financing costs on group level,

•

Improvement of investment return due to economies of scale,

•

Simplification of liquiditymanagagement on local level,

•

Reduction of external banking costs due to centralization,

•

Optimization of cash flow forecast because of coordination of

financing cycles,

•

Break-Even of a cash pool starts at around 300’000.- required

capital.

Contact us, we would be glad to show you the possible

opportunities!

debt and increase the available liquidity. Furthermore, especially

interest benefits in multiple ways can be achieved for the pool

participants on the payable and on the receivable side.

Type 1: Zero- or Target Balancing Cash Pool

(physical)

The zero-balancing, also called cash-concentration or sweeping, is

in his form the easiest way to introduce cash pooling. Depending on a

surplus or lack of cash, all cash balances in the Pool (Pool-

Participants) will be transferred on daily basis automatic to or from

the top-mother account (Pool-Leader). A major positive effect is a

shorter balance and therefore the key-figure of the debt-ratio

improves. But there are also some disadvantages, e.g. liability-

questions in case of a short-fall of the pool-leader (see Erb-Group

and Swissair in Switzerland or Bremer Vulkan in Germany). Also

there is a higher administrative work since all intercompany cash

flows on a daily level have to be booked at the pool-leader (can be

automatized). The key-element of a zero- or target balancing is that

all cash flows are physicly.

Setup of a Zero-Balancing-Pool

It is also important to respect tax considerations, i.e. transfer pricing.

Because as already mentioned, the “classic” cash pooling is simply

an automatic loan transaction on daily basis. Some countries, also

in Europe, have laws that either interest payment and/or loans in the

one or other direction are prohibited or even do not allow physical

cash flows. This is typically a process of multinational groups and has

negative impact on cross border transactions.

Process / Functionality of a Zero- or Target Cash Pool

Pooling Accounts of the Participants can be regulated in two ways,

both fully automatic:

a) Zero-Balancing: all participating accounts, except the header-

account, are set to 0 (zero) at the end of a day. Surplus balances are

debited, minus balances are credited to/from the header account.

b) Target-Balancing: basically the same procedure as with zero-

balancing, just with a number of extended parameter regarding the

day-end balance. For example every day a pre-defined balance

remain on the account, which may be for instance used for lease-

guarantee etc.

Because of technical restrictions all transfers can be booked at the

next following day, but will be execured always with the correct value

date.

Here an example, how the communications for the transfer of

balances may happen through the SWIFT-Network. Dependent from

the executing Banks some differences can be the case. It is also

often the case that the cash pool can be not managed by only one

Bank, because the House-Bank has not in every country a branch.

This is commonly the case in Cross-Border Pools, see below. That

means a third Bank must be included in the pool-network.

This example is certainly strong simplified und contains for instance

no internal connections which are mandatory in the accounting of the

Pool-Leader an all Subsidiaries.

Type 2: Notional Cash Pool

(no physical transfer of funds)

The meaning of „notional“ name it: this pooling form is not real. But is

is a 100% interest optimization. There are no physical transfers

between the accounts. The single balance accounts will be added

together and netted against each other. Therefore each pool

participant has his own bankaccount with the full physical balance,

but the full interest spread remain within the group.

Therefore this kind of pooling meets perfect the needs of companies

which does not like to enter into any credit risk! In a few words:

interest optimization without having the character of loans and related

risks.

An extended version of this pooling is a combination of different

currencies in one and the same cash-pool. Some Banks offer this

service, ask us for assistance. Technically, the Bank is just entereing

into a number of overnight-swaps.

Complex Topic: Cross Border Cash Pooling

A well tuned cash pool structure may not only transfer cash over the

border, it can do it even in different currencies! So it is possible to

establish a cash pool for EUR, one for for CHF and one for USD. All

cash flows will be transferred to / from the ultimate mother group

account on daily basis and will be managed by the Treasurer as

portfolio to cover gaps on daily or weekly with swaps, without

entering into any foreign exchange risk!

Cross-Border Pooling is certainly the biggest advantage for a cash

management who wants to generate a maximum benefit out of the

cash pool. But also the risk increase and therewith related, the

ultimate accuracy for setting up or manage cross-border pools. Risk

has per definition the attribute as getting larger as more parameters

need to be considered. The adavantages and disadvantages are

different from company to company, depending on the structure and

planned pooling type. For instance, the right bank on your side is very

important. To find out who this bank could be is described here. In the

the following just a view arguments in a SWOT analysis which should

be considered very carefully:

Controlling

Be aware - cash pooling can be also a threat if rights and liabilites are

not clearly defined. For this we recommend a comprehensive Treasuy

Policy - see here.

Software Support

A proper management of a cash pooling may become quite complex

if there is no sufficient support by an adequated software. See here

how Cash Pooling can be managed easy and safe with the Cash Pool

Module in our Treasury Software STS.

Country specific Items

Depending on the country where the bank-account for the cash pool

is established, it is fully, partially or not allowed to operate such a

pool. Based on our experience with cash pool projects world wide we

composed a manuscript which gives an overview about the different

country-specifications. Read more in detail here.

Reasons for Cash Pooling

Optimal allocation of internal liquid funds and max. reduction of

external debts,

•

Reduction of financing costs on group level,

•

Improvement of investment return due to economies of scale,

•

Simplification of liquiditymanagagement on local level,

•

Reduction of external banking costs due to centralization,

•

Optimization of cash flow forecast because of coordination of

financing cycles,

•

Break-Even of a cash pool starts at around 300’000.- required

capital.

Contact us, we would be glad to show you the possible

opportunities!