Individual Ranking of Banks

Standard Ranking (S&P, Fitch etc.) is common ranking practice -but it cannot match all

your requirements to a Bank!

Up until end of 2007 many banks had the untouchable reputation that there is no doubt about that they are the best experts regarding safety. If anybody likes to ask for counterparty risk then it was always the bank who declined a request for funds due to reasons of reliability. But now the

customer should also take this position, it may be even a matter of his existence. Doing business with the wrong bank may lead to total loss of

liquidity. Easier told as done - but how how can one rate his current and/or desired bank?

The one who has the money is right. This anrupt conclusion was in the past (and is mostly still fact) the lived understanding of most heads of

individuals which have the power of dealing with money - and they do it as it would be their own money. That’s obviously the reason for “a golden

key can open any door”. Plot-wise this money is not their property, they just administer it. In fact they have the same amount as liabilities by

collecting money from other people / organsations. That’s not the same as it is for every corporate outside the banking business. It’s just a transfer

from one person to the other and getting a margin for.

Rating of a Bank

Before you can make a rating it is important to get a customer-supplier view, free of emotions and all the time critical challenged whether the

earned experience is correct resp. whether they are still actual. That’s the reason for the (allowedly little bit provocating) introducing explanations

which should make someone aware of trust in overall simple things.

Example

The bank to be rated has good or very good rating at the well known rating agencies Standard & Poors, Moody's or Fitch.

1.

Is this rating for a specific bond or really a overall credit-rating?

2.

Is the rating for the whole banking organsiation / group or is it just for a part of it, e.g. a single country or segment?

3.

How old is the rating? If it is older than a year you should better renounce it.

4.

If you buy any product from bank, is it really from you bank and not from another one, rated very much worser? Remind on practical

examples, e.g. Credit Suisse vs. Lehman Brothers? They sold Lehman products, but the customer thought that ge made an investment at

Credit Suisse. In fact, the customer lost everything when Lehman went bankcrupt suddenly over night!

That means, is the rating in fact what you are interested for, i.e. does it belongs to your business? If you don’t have a current and important,

suitable rating, but also for every other rating for fully transparent analysis, you see below a proven approach to rate your current or future bank.

Under all circumstances you should make your own personal analysis for a current existing rating. As you can see below, such an

analysis can never be substituted by a general one.

Segmentation

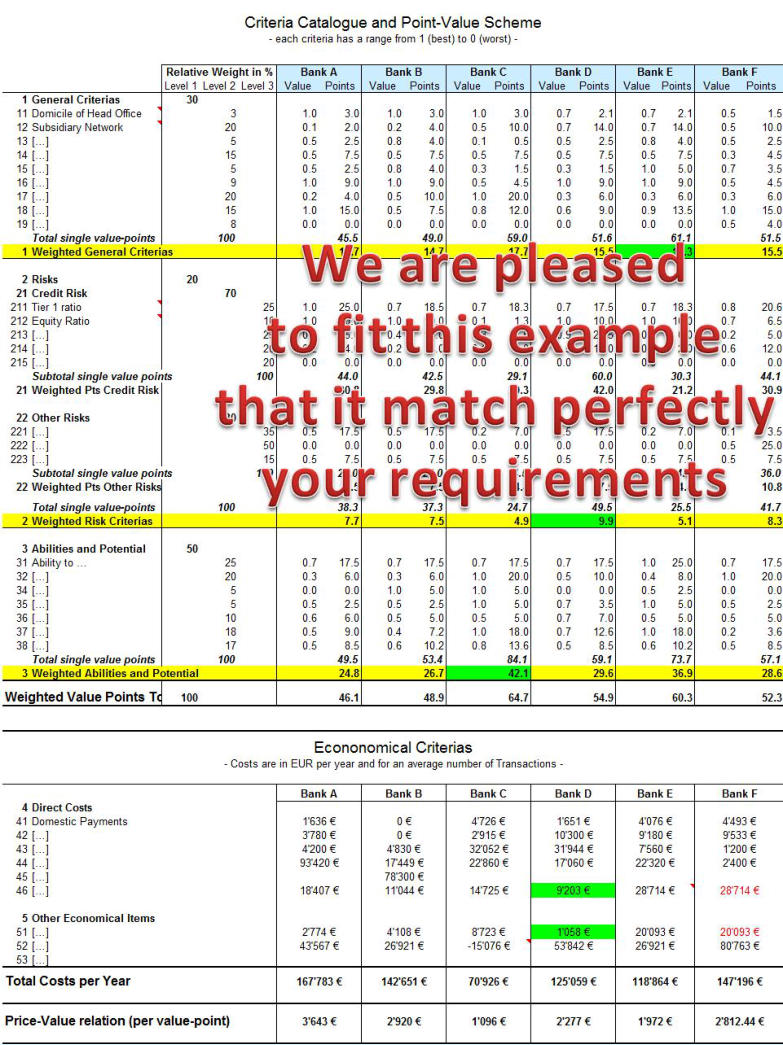

The result should be a cost-benefit analysis (i.e. two dimensions) which is segregated in general criterias, risk and potential. Ideally, a SWOT

analysis was made before.

anybody likes to ask for counterparty risk then it was always the bank who declined a request for funds due to reasons of reliability. But now the

customer should also take this position, it may be even a matter of his existence. Doing business with the wrong bank may lead to total loss of

liquidity. Easier told as done - but how how can one rate his current and/or desired bank?

The one who has the money is right. This anrupt conclusion was in the past (and is mostly still fact) the lived understanding of most heads of

individuals which have the power of dealing with money - and they do it as it would be their own money. That’s obviously the reason for “a golden

key can open any door”. Plot-wise this money is not their property, they just administer it. In fact they have the same amount as liabilities by

collecting money from other people / organsations. That’s not the same as it is for every corporate outside the banking business. It’s just a transfer

from one person to the other and getting a margin for.

Rating of a Bank

Before you can make a rating it is important to get a customer-supplier view, free of emotions and all the time critical challenged whether the

earned experience is correct resp. whether they are still actual. That’s the reason for the (allowedly little bit provocating) introducing explanations

which should make someone aware of trust in overall simple things.

Example

The bank to be rated has good or very good rating at the well known rating agencies Standard & Poors, Moody's or Fitch.

1.

Is this rating for a specific bond or really a overall credit-rating?

2.

Is the rating for the whole banking organsiation / group or is it just for a part of it, e.g. a single country or segment?

3.

How old is the rating? If it is older than a year you should better renounce it.

4.

If you buy any product from bank, is it really from you bank and not from another one, rated very much worser? Remind on practical

examples, e.g. Credit Suisse vs. Lehman Brothers? They sold Lehman products, but the customer thought that ge made an investment at

Credit Suisse. In fact, the customer lost everything when Lehman went bankcrupt suddenly over night!

That means, is the rating in fact what you are interested for, i.e. does it belongs to your business? If you don’t have a current and important,

suitable rating, but also for every other rating for fully transparent analysis, you see below a proven approach to rate your current or future bank.

Under all circumstances you should make your own personal analysis for a current existing rating. As you can see below, such an

analysis can never be substituted by a general one.

Segmentation

The result should be a cost-benefit analysis (i.e. two dimensions) which is segregated in general criterias, risk and potential. Ideally, a SWOT

analysis was made before.

anybody likes to ask for counterparty risk then it was always the bank who declined a request for funds due to reasons of reliability. But now the

customer should also take this position, it may be even a matter of his existence. Doing business with the wrong bank may lead to total loss of

liquidity. Easier told as done - but how how can one rate his current and/or desired bank?

The one who has the money is right. This anrupt conclusion was in the past (and is mostly still fact) the lived understanding of most heads of

individuals which have the power of dealing with money - and they do it as it would be their own money. That’s obviously the reason for “a golden

key can open any door”. Plot-wise this money is not their property, they just administer it. In fact they have the same amount as liabilities by

collecting money from other people / organsations. That’s not the same as it is for every corporate outside the banking business. It’s just a transfer

from one person to the other and getting a margin for.

Rating of a Bank

Before you can make a rating it is important to get a customer-supplier view, free of emotions and all the time critical challenged whether the

earned experience is correct resp. whether they are still actual. That’s the reason for the (allowedly little bit provocating) introducing explanations

which should make someone aware of trust in overall simple things.

Example

The bank to be rated has good or very good rating at the well known rating agencies Standard & Poors, Moody's or Fitch.

1.

Is this rating for a specific bond or really a overall credit-rating?

2.

Is the rating for the whole banking organsiation / group or is it just for a part of it, e.g. a single country or segment?

3.

How old is the rating? If it is older than a year you should better renounce it.

4.

If you buy any product from bank, is it really from you bank and not from another one, rated very much worser? Remind on practical

examples, e.g. Credit Suisse vs. Lehman Brothers? They sold Lehman products, but the customer thought that ge made an investment at

Credit Suisse. In fact, the customer lost everything when Lehman went bankcrupt suddenly over night!

That means, is the rating in fact what you are interested for, i.e. does it belongs to your business? If you don’t have a current and important,

suitable rating, but also for every other rating for fully transparent analysis, you see below a proven approach to rate your current or future bank.

Under all circumstances you should make your own personal analysis for a current existing rating. As you can see below, such an

analysis can never be substituted by a general one.

Segmentation

The result should be a cost-benefit analysis (i.e. two dimensions) which is segregated in general criterias, risk and potential. Ideally, a SWOT

analysis was made before.

The weighted points are now set in comparison to the total costs. Due to this, a meaningful graphic analyis about the cost-benefits can be made.

regarding a future bank relationship. As an example, the graphs my look like the ones below:

regarding a future bank relationship. As an example, the graphs my look like the ones below:

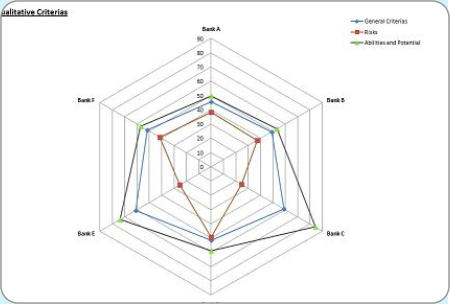

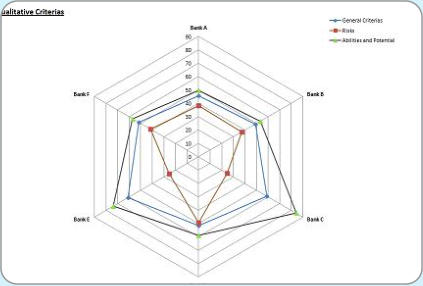

Qualitative

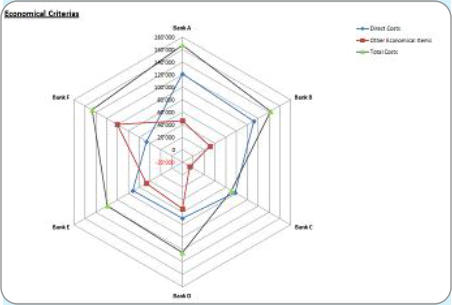

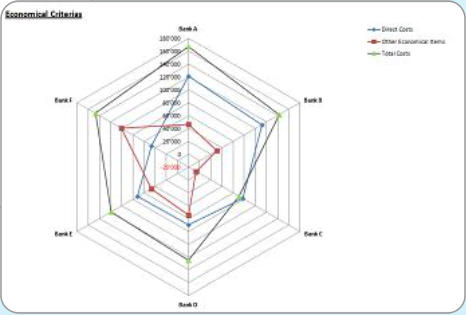

Economical

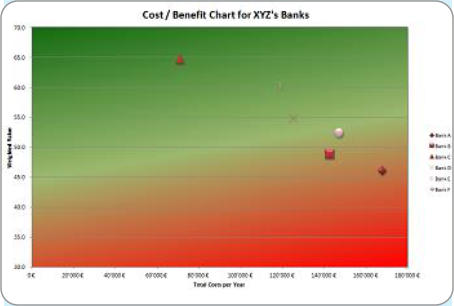

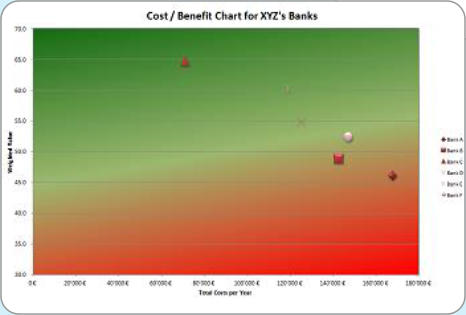

Cost-Benefit

With this analysis you are able now to segregate the

expensive ones with poor performance from the ones

with more competitive prices and better offers. You

can now invite the 2 - 3 best banks for a personal

meeting. The bank will now show clear more respect

and makes more concessions, if you show them from

the beginning that you are interested in a very

professional relationship and that you are able to

manage your business well. Because the bank is your

vendor and you her customer. Same like in your

operational business you rely on one of the very most

important points in a business: CONFIDENCE.

expensive ones with poor performance from the ones

with more competitive prices and better offers. You

can now invite the 2 - 3 best banks for a personal

meeting. The bank will now show clear more respect

and makes more concessions, if you show them from

the beginning that you are interested in a very

professional relationship and that you are able to

manage your business well. Because the bank is your

vendor and you her customer. Same like in your

operational business you rely on one of the very most

important points in a business: CONFIDENCE.

Contact us, we would be glad to show you the possible opportunities!

Individual Ranking of Banks

Standard Ranking (S&P, Fitch etc.) is common ranking practice

-but it cannot match all your requirements to a Bank!

Up until end of 2007 many banks had the untouchable reputation

that there is no doubt about that they are the best experts regarding

safety. If anybody likes to ask for counterparty risk then it was always

the bank who declined a request for funds due to reasons of

reliability. But now the customer should also take this position, it may

be even a matter of his existence. Doing business with the wrong

bank may lead to total loss of liquidity. Easier told as done - but how

how can one rate his current and/or desired bank?

The one who has the money is right. This anrupt conclusion was in

the past (and is mostly still fact) the lived understanding of most

heads of individuals which have the power of dealing with money -

and they do it as it would be their own money. That’s obviously the

reason for “a golden key can open any door”. Plot-wise this money is

not their property, they just administer it. In fact they have the same

amount as liabilities by collecting money from other people /

organsations. That’s not the same as it is for every corporate outside

the banking business. It’s just a transfer from one person to the other

and getting a margin for.

Rating of a Bank

Before you can make a rating it is important to get a customer-

supplier view, free of emotions and all the time critical challenged

whether the earned experience is correct resp. whether they are still

actual. That’s the reason for the (allowedly little bit provocating)

introducing explanations which should make someone aware of trust

in overall simple things.

Example

The bank to be rated has good or very good rating at the well known

rating agencies Standard & Poors, Moody's or Fitch.

1.

Is this rating for a specific bond or really a overall credit-rating?

2.

Is the rating for the whole banking organsiation / group or is it

just for a part of it, e.g. a single country or segment?

3.

How old is the rating? If it is older than a year you should better

renounce it.

4.

If you buy any product from bank, is it really from you bank and

not from another one, rated very much worser? Remind on

practical examples, e.g. Credit Suisse vs. Lehman Brothers?

They sold Lehman products, but the customer thought that ge

made an investment at Credit Suisse. In fact, the customer lost

everything when Lehman went bankcrupt suddenly over night!

That means, is the rating in fact what you are interested for, i.e. does

it belongs to your business? If you don’t have a current and

important, suitable rating, but also for every other rating for fully

transparent analysis, you see below a proven approach to rate your

current or future bank.

Under all circumstances you should make your own personal

analysis for a current existing rating. As you can see below,

such an analysis can never be substituted by a general one.

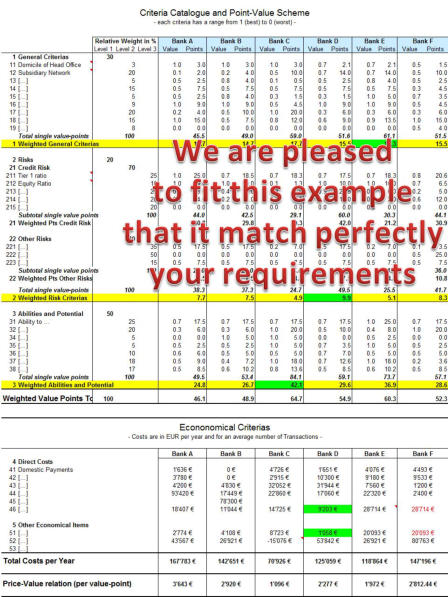

Segmentation

The result should be a cost-benefit analysis (i.e. two dimensions)

which is segregated in general criterias, risk and potential. Ideally, a

SWOT analysis was made before.

The weighted points are now set in comparison to the total costs. Due to

this, a meaningful graphic analyis about the cost-benefits can be made.

regarding a future bank relationship. As an example, the graphs my look

like the ones below:

Qualitative

Economical

Cost-Benefit

With this analysis you are able now to segregate the expensive ones

with poor performance from the ones with more competitive prices

and better offers. You can now invite the 2 - 3 best banks for a

personal meeting. The bank will now show clear more respect and

makes more concessions, if you show them from the beginning that

you are interested in a very professional relationship and that you are

able to manage your business well. Because the bank is your vendor

and you her customer. Same like in your operational business you

rely on one of the very most important points in a business:

CONFIDENCE.

Contact us, we would be glad to show you the possible

opportunities!

that there is no doubt about that they are the best experts regarding

safety. If anybody likes to ask for counterparty risk then it was always

the bank who declined a request for funds due to reasons of

reliability. But now the customer should also take this position, it may

be even a matter of his existence. Doing business with the wrong

bank may lead to total loss of liquidity. Easier told as done - but how

how can one rate his current and/or desired bank?

The one who has the money is right. This anrupt conclusion was in

the past (and is mostly still fact) the lived understanding of most

heads of individuals which have the power of dealing with money -

and they do it as it would be their own money. That’s obviously the

reason for “a golden key can open any door”. Plot-wise this money is

not their property, they just administer it. In fact they have the same

amount as liabilities by collecting money from other people /

organsations. That’s not the same as it is for every corporate outside

the banking business. It’s just a transfer from one person to the other

and getting a margin for.

Rating of a Bank

Before you can make a rating it is important to get a customer-

supplier view, free of emotions and all the time critical challenged

whether the earned experience is correct resp. whether they are still

actual. That’s the reason for the (allowedly little bit provocating)

introducing explanations which should make someone aware of trust

in overall simple things.

Example

The bank to be rated has good or very good rating at the well known

rating agencies Standard & Poors, Moody's or Fitch.

1.

Is this rating for a specific bond or really a overall credit-rating?

2.

Is the rating for the whole banking organsiation / group or is it

just for a part of it, e.g. a single country or segment?

3.

How old is the rating? If it is older than a year you should better

renounce it.

4.

If you buy any product from bank, is it really from you bank and

not from another one, rated very much worser? Remind on

practical examples, e.g. Credit Suisse vs. Lehman Brothers?

They sold Lehman products, but the customer thought that ge

made an investment at Credit Suisse. In fact, the customer lost

everything when Lehman went bankcrupt suddenly over night!

That means, is the rating in fact what you are interested for, i.e. does

it belongs to your business? If you don’t have a current and

important, suitable rating, but also for every other rating for fully

transparent analysis, you see below a proven approach to rate your

current or future bank.

Under all circumstances you should make your own personal

analysis for a current existing rating. As you can see below,

such an analysis can never be substituted by a general one.

Segmentation

The result should be a cost-benefit analysis (i.e. two dimensions)

which is segregated in general criterias, risk and potential. Ideally, a

SWOT analysis was made before.

The weighted points are now set in comparison to the total costs. Due to

this, a meaningful graphic analyis about the cost-benefits can be made.

regarding a future bank relationship. As an example, the graphs my look

like the ones below:

Qualitative

Economical

Cost-Benefit

With this analysis you are able now to segregate the expensive ones

with poor performance from the ones with more competitive prices

and better offers. You can now invite the 2 - 3 best banks for a

personal meeting. The bank will now show clear more respect and

makes more concessions, if you show them from the beginning that

you are interested in a very professional relationship and that you are

able to manage your business well. Because the bank is your vendor

and you her customer. Same like in your operational business you

rely on one of the very most important points in a business:

CONFIDENCE.

Contact us, we would be glad to show you the possible

opportunities!